The Inverter Is No Longer Just a Box on the Wall

Ask anyone in the solar industry what the most important component of a solar power system is, and you will almost certainly hear the same answer: the solar panel. That answer was probably correct a decade ago. In 2027, it is no longer the full picture.

The solar inverter – the device responsible for converting the direct current electricity that solar panels produce into the alternating current that homes, factories, and grids actually use – has undergone a fundamental transformation over the past five years. What was once a straightforward power electronics box has evolved into an intelligent energy management platform that simultaneously optimizes solar generation, manages battery storage, monitors grid conditions in real time, supports electric vehicle charging, and communicates performance data to cloud-based analytics systems.

This evolution has changed everything about how inverters are bought, specified, and evaluated – and it has reshuffled the competitive landscape among the companies that make them more dramatically than at any previous point in the industry’s history. The Solar PV Inverters Market has transitioned from a component-driven industry into a strategically integrated power electronics ecosystem where software intelligence, grid interaction capability, and operational reliability increasingly determine competitive positioning.

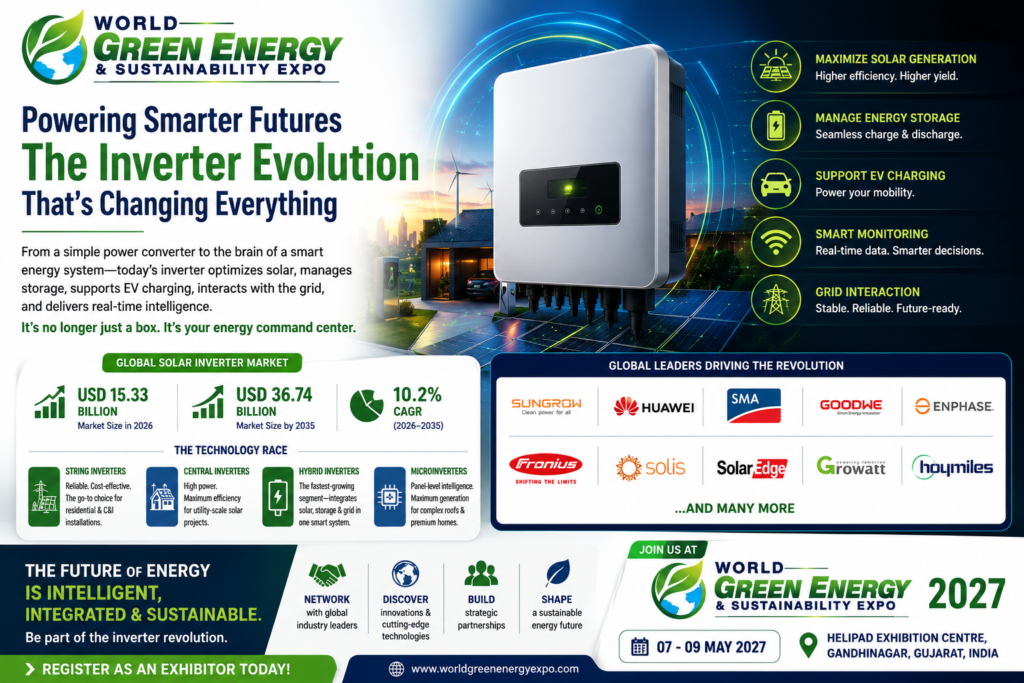

The global solar inverter market is valued at USD 15.33 billion in 2026 and is projected to reach USD 36.74 billion by 2035 at a CAGR of 10.2%. For inverter manufacturers, system integrators, rooftop solar installers, utility-scale developers, and procurement engineers, understanding where this market is heading – and which technology is winning – is no longer optional background knowledge. It is a strategic requirement.

The Global Solar Inverter Market in 2027 – Size, Growth and Key Drivers

Solar inverter market valuations vary across research houses depending on which product categories they include, but every credible source points in the same direction – strong, sustained growth through the rest of this decade and into the next. The global solar inverter market size is estimated at USD 22,502 million in 2026 and is projected to reach USD 48,405 million by 2035, growing at a CAGR of 8.9%. The global solar PV inverters market size was estimated at USD 15.8 billion in 2025 and is projected to reach USD 31.7 billion by 2035, growing at a CAGR of 7.2% from 2026 to 2035.

The underlying demand driver is straightforward. Global installation of solar PV systems reached over 100 GW in 2022, with solar inverter units playing a significant role in these installations. The demand for solar inverters has increased substantially due to rising focus on renewable energy and supportive government policies globally. Key market driver – demand for grid-connected systems keeps climbing as installation volumes crossed nearly 240 GW globally last year, pushing manufacturers to scale faster than they expected.

However, growth is not uniform and the competitive environment is intensifying. Analysts expect a 2% decline in global inverter demand by the end of 2025, followed by a further 9% contraction in 2026. The main drivers are regulatory and incentive changes affecting solar markets in China, Europe, and the United States. This demand softness in mature markets is creating intense pricing pressure that is separating financially resilient manufacturers from weaker players – accelerating consolidation across the global supply chain.

Innovation has become a core pillar of investment strategies. High-performance products alone are no longer sufficient. Manufacturers must continuously invest in research and development, accelerate technology upgrades, and adapt to shifting demand patterns. In an increasingly protectionist policy environment, localized production has also become a key competitive factor.

Emerging trends include hybrid inverters picking up traction, with over 15% of new residential systems now combining storage-ready setups, while smart monitoring units surpassed 20 million active deployments. Asia-Pacific leads, installing over 120 GW of solar capacity in a single year, which naturally drives the highest inverter consumption across any region.

String vs Central vs Hybrid vs Microinverter – The Technology Battle Explained

This is the question at the heart of every procurement decision in the solar inverter market. The answer is not simple, because each technology is genuinely superior in specific applications – and the market is actively moving in all three directions simultaneously, just across different segments.

String Inverters – The Volume Leader

String solar inverters is the largest segment of the global solar inverter market due to the rapidly growing residential solar market, the global shift towards renewable energy sources, high market availability, low initial investment of string inverters, the rise of smart grid technology, and ongoing advancements in string inverter technology such as higher efficiency ratings, greater durability, and enhanced monitoring capabilities. String inverters are ideal for commercial and residential applications, including modest utility installations of less than 1 MW. String inverters are ideal for households seeking low-cost PV systems or for properties with simple roofs and constant renewable electricity throughout the day.

The core principle of a string inverter is simple: solar panels are connected in series – a string – and the combined DC output of that string flows into a single inverter that converts it to AC. The system is cost-effective, reliable, and well-understood by installers and maintenance technicians. Modern string inverters have reached efficiency levels above 98.5% and incorporate sophisticated MPPT algorithms, fault detection, and cloud monitoring – capabilities that only premium central inverters offered a decade ago.

The primary limitation of string inverters is their sensitivity to partial shading and panel mismatch. If one panel in a string underperforms, the entire string’s output is reduced. This is manageable on simple, unobstructed roofs with consistent sun exposure, but becomes a meaningful yield penalty on complex rooftops with chimneys, skylights, or trees nearby.

Central Inverters – The Utility-Scale Workhorse

The global central PV inverter market is expected to reach USD 24.80 billion by 2033 from USD 14.50 billion in 2025, at a CAGR of 6.60% from 2026 to 2033. The 1,000-kW segment is projected to witness the highest CAGR in the central PV inverter market during the forecast period. In the utility-scale solar project market, the dominant PV inverter configuration has been high-capacity central inverters with ratings greater than 1,000 kW. These types of inverters serve as an effective solution to provide maximum available efficiency and reliability in addition to providing stability to the electric utility grid.

Central inverters aggregate the DC output of large arrays – hundreds or thousands of panels – into a single high-power conversion unit. Their key advantages at utility scale are lower cost per watt of conversion capacity, simpler wiring infrastructure across large sites, and easier grid-interface management through a single point of interconnection. Smart technologies like digital monitoring, AI-based fault analysis, and hybrid integration with energy storage systems can significantly improve project controllability and predictability. Manufacturers of high-capacity central inverters are continuing to provide innovative solutions such as predictive maintenance capabilities, remote diagnostics, and digital optimization to improve reliability and maximize ROI.

The direction of travel in central inverters is unmistakably toward higher power – systems exceeding 5 MW at a single unit are now commercially available. The market shows signs of evolving toward more powerful inverters that surpass 400 kW to reduce costs and enhance operational efficiency in utility-scale installations. The implementation of 2,000-volt inverters shows potential to extend solar panel arrays while enabling substantial savings in balance-of-system spending.

Hybrid Inverters – The Fastest-Growing Segment

If string inverters are the volume leader and central inverters are the utility-scale workhorse, hybrid inverters are unambiguously the technology with the most commercial momentum in 2027.

The solar hybrid inverter market was valued at USD 10,101 million in 2025 and is expected to reach USD 25,904 million by 2032, growing at a CAGR of 14.4%. Close to 45% of solar energy projects now rely on hybrid inverters to balance energy between solar panels, storage units, and the grid. Their ability to provide seamless backup power and cost efficiency makes them highly attractive across diverse energy applications. Around 50% of modern solar installations are integrating hybrid inverters, strongly driven by the need for reliable storage.

Global solar installations exceeded 1.4 terawatts, with hybrid inverter adoption accelerating in residential, commercial, and industrial applications due to rising grid instability and peak-load challenges. More than 55% of new rooftop solar systems now integrate hybrid inverter configurations to support battery readiness. A hybrid inverter combines three functions in a single unit: solar generation management, battery charge and discharge control, and grid interaction. This integration eliminates the need for separate charge controllers and battery inverters, reducing system cost and complexity while enabling far more sophisticated energy management – time-of-use optimization, backup power during outages, demand response participation, and grid export management – from a single device.

The industry is shifting from standalone string inverters to AI-managed hybrid systems that integrate battery storage, EV charging, and grid services. In February 2026, Sungrow announced plans to open its first factory in Europe to strengthen local manufacturing capabilities. High-efficiency models can improve energy output by 2 to 6%, while hybrid inverters with storage capabilities can cut electricity costs by up to 60% through time-of-use optimization.

Microinverters – The Premium Residential Option

Microinverters solve the string inverter’s shading problem by placing a small individual inverter directly on each solar panel, converting DC to AC at the panel level. This panel-level independence eliminates the performance drag that shading or panel mismatch creates in string systems, making microinverters the highest-yield option for complex rooftops.

In June 2024, Enphase unveiled the IQ8X and IQ8P microinverters engineered for next-generation high-powered solar modules up to 670W DC, reflecting the continuous push toward higher power handling within the microinverter form factor. Microinverters’ higher upfront cost limits their adoption to premium residential and commercial markets – primarily the United States, Australia, and parts of Europe – where yield optimization and panel-level monitoring justify the price premium.

Answer: Which Solar Inverter Technology Is Winning?

The honest answer is that no single technology is winning across all segments simultaneously. Each is winning in its own domain, and the boundaries between domains are shifting:

String inverters are winning on volume, driven by residential and small commercial solar growth.

Central inverters are winning on power – moving to ever-larger unit sizes as utility-scale projects grow in scale.

Hybrid inverters are winning on growth rate – 14.4% CAGR versus 6 to 8% for pure string or central – because the integration of storage is becoming the default expectation rather than an optional add-on.

Microinverters are winning on yield and monitoring in premium residential markets where per-kilowatt-hour economics justify the cost.

The single most consequential trend in this landscape is the convergence between string inverters and hybrid inverters. Across the residential and commercial segments, the question is no longer “should I buy a string inverter or a hybrid inverter?” – it is increasingly “how soon will I add storage to this system, and should I buy a hybrid-ready inverter now so I do not have to replace it when I do?”

The Global Rankings – Who Is Leading the Solar Inverter Industry in 2027

The solar inverter competitive landscape has consolidated around a small number of dominant manufacturers while simultaneously fragmenting in regional and niche segments. The definitive reference for global inverter rankings comes from Wood Mackenzie’s Global Solar Inverter Manufacturer Rankings, updated in 2026.

Sungrow and Huawei retained the top position in Wood Mackenzie’s 2026 Global Solar Inverter Manufacturer Ranking for the second consecutive year, as developers, investors, and lenders place increasing emphasis on manufacturing diversification, cybersecurity readiness, and long-term operational reliability when selecting inverter suppliers. The ranking places Germany’s SMA at third, while China’s GoodWe and the USA’s Enphase completed the top five. Hoymiles in sixth and APSystems in tenth entered the top ten for the first time. The remainder of the top ten includes China’s Ginlong Solis at seventh, Israel’s SolarEdge at eighth, Austria’s Fronius at ninth, and China’s Aiswei/Solplanet at joint tenth.

Huawei and Sungrow were the only manufacturers to meet all eight benchmark criteria assessed in the ranking, distinguishing themselves through strong performance across research and development, manufacturing diversification, global service coverage, and financial strength. Twenty-one manufacturers achieved Wood Mackenzie’s Grade A designation in 2026, reflecting continued improvement in transparency, operational capability, and service quality across the global inverter industry.

Here is the complete profile of each leading company:

Huawei Digital Power (China)

Huawei’s strength is not limited to inverter manufacturing. With its background in digital technology, smart PV platforms, and energy storage integration, Huawei can provide complete solar energy solutions for different project types. Its technology supports diverse needs with a focus on long-term reliability and smart automation. Huawei’s solutions are widely used in residential rooftops for energy savings and self-consumption, in commercial and industrial settings for system scalability and intelligent control, and in utility-scale plants for grid support and low operational costs.

Huawei’s FusionSolar smart PV platform – combining string inverters, optimizers, and cloud-based AI analytics – is arguably the most comprehensive solar energy management ecosystem deployed at scale anywhere in the world. The company’s dominant position in the Chinese market, combined with major international project presence in the Middle East, Southeast Asia, and Africa, gives it a scale advantage that competitors find very difficult to match.

Sungrow Power Supply (China)

Sungrow is one of the most influential solar inverter and energy storage system manufacturers in the world. Founded in 1997 in China, the company has built a strong presence across PV inverters, energy storage systems, floating PV solutions, EV charging, wind products, and hydrogen equipment. Its products and solutions serve homeowners, commercial and industrial users, utility-scale power plants, EPC companies, installers, and energy developers. With over 740 GW of installed capacity worldwide, the company has earned a reputation for delivering reliable and adaptable solar power solutions.

Sungrow’s strategic breadth – spanning residential string inverters through to utility-scale central inverters, grid-scale BESS, EV chargers, and hydrogen equipment – makes it one of the most comprehensively diversified clean energy technology companies in the world. Its 105% revenue growth in energy storage in 2025, combined with its established inverter leadership, positions it as the single most dangerous competitive force in the broader solar-plus-storage integration market.

SMA Solar Technology (Germany)

SMA Solar Technology is a long-established German solar inverter manufacturer with roots dating back to 1981. Headquartered in Niestetal, Germany, SMA has built its reputation on engineering quality, stable product performance, and long-term system reliability. In 2025, SMA Solar Technology advanced utility-scale inverter systems featuring enhanced grid-support functionality and dynamic voltage regulation capability, aligning with growing regulatory requirements for renewable-heavy power networks requiring advanced grid interaction performance. In September 2025, SMA Solar partnered with Create Energy to manufacture Sunny High-power PEAK3 inverters at a Tennessee facility under USA domestic content incentives.

SMA’s European heritage and decades-long track record give it a bankability advantage in European project finance – lenders and insurers who have seen SMA inverters perform reliably for 20-plus years in the field are more comfortable extending long-duration project financing to SMA-specified systems than to newer market entrants.

Fronius (Austria)

Fronius is the premium European residential and commercial inverter brand, known for exceptional build quality, reliability, and one of the most comprehensive service networks of any inverter manufacturer in Europe and Australia. Its Symo and Primo series are widely specified across European residential and commercial markets. Fronius’s strength in quality and service has allowed it to maintain premium pricing and strong installer loyalty even as Chinese competitors have driven down entry-level inverter prices dramatically.

GoodWe (China)

GoodWe is a publicly listed company and one of the most prominent players in the smart energy industry. With a global presence spanning over 100 countries, the company provides solar power inverters and energy storage systems for both residential and commercial markets. GoodWe has built its reputation by combining efficient power electronics with intelligent software platforms, creating solutions that are not only reliable but also easy to monitor and control. GoodWe is a flexible choice for users who need different inverter options across multiple project types, with products covering inverters from 0.7 kW to 350 kW.

GoodWe’s rise to fifth place in the 2026 Wood Mackenzie rankings – up from sixth in H1 2025 – reflects its successful expansion beyond China into European, Indian, and Southeast Asian markets, where its combination of competitive pricing, wide product range, and improving service infrastructure has made it one of the most rapidly gaining brands in the mid-market segment.

Enphase Energy (USA)

In 2026, Enphase Energy accelerated expansion of integrated residential energy ecosystems by advancing hybrid inverter and battery management interoperability designed to support home energy optimization and backup power continuity under distributed energy deployment models. Enphase dominates the North American premium residential microinverter market with a position so entrenched that it is essentially the default specification for premium US residential solar installations. Its IQ8 series – capable of operating independently of the grid – addresses one of the most consistent consumer concerns in markets with unreliable grid power.

Ginlong / Solis (China)

In January 2025, Solis launched its revolutionary Solarator Series, a hybrid inverter designed to address diverse energy challenges. Ginlong Solis has built a strong global distribution network for its string and hybrid inverters, with particularly strong penetration in the Indian market where its competitive pricing and reliable technical support have made it a leading choice for rooftop solar installers.

SolarEdge Technologies (Israel)

In 2025, SolarEdge Technologies strengthened its commercial and industrial inverter portfolio through expanded AI-enabled monitoring and predictive maintenance functionality intended to improve energy yield management and operational reliability across distributed solar installations. SolarEdge’s DC-optimized inverter architecture – combining string inverters with module-level power optimizers rather than traditional microinverters – delivers microinverter-level yield optimization at a lower cost per watt. After a financially difficult period in 2024 and early 2025, SolarEdge is rebuilding its commercial momentum through its strengthened C&I portfolio and expanding energy storage offering.

Growatt (China)

Growatt is a fast-growing solar power inverter manufacturer recognized for combining affordability with reliable performance, especially in residential and emerging market applications. Since its founding, the company has expanded into over 160 countries, offering a full range of PV inverters, energy storage systems, and smart energy management solutions. Growatt solutions are widely used in residential rooftops, rural electrification, and small-scale commercial systems. The brand is especially favored by users seeking cost-effective systems with intuitive interfaces and mobile connectivity. Its hybrid inverters provide strong value in off-grid villages, backup power applications, and solar-powered homes in regions with limited utility infrastructure.

Growatt has emerged as the dominant inverter brand in India’s price-sensitive residential rooftop market, combining competitive pricing with a strong national distributor network and BIS-certified product range that meets MNRE requirements for government-supported installations.

Hoymiles (China)

Hoymiles entered the top ten for the first time in the 2026 Wood Mackenzie rankings. Hoymiles specializes in microinverters and rapid shutdown solutions, having built a strong position in European and North American residential markets as the leading alternative to Enphase for installers seeking microinverter technology at more competitive price points.

India’s Solar Inverter Market – A Growing Opportunity

India’s solar inverter market is a direct function of its solar installation pace – and with 7.1 GW of rooftop solar installed in 2025 and 45 GW of total solar added in FY 2025-26, inverter demand is growing at a pace that is attracting investment from virtually every major global manufacturer. India accounts for fourth position in renewable energy capacity installation. India is an opportunistic market for solar hybrid inverter companies backed by supportive government policies and schemes. The PM-KUSUM Scheme is effectively assisting farmers to install solar power plants, solarise grid-connected agriculture pumps, and standalone solar agriculture pumps by offering financial assistance.

The residential market, powered by PM Surya Ghar, is creating enormous demand for 1 kW to 10 kW string and hybrid inverters across India’s residential rooftop segment. The rapid shift toward hybrid inverters in new residential installations – driven by homeowners wanting backup power alongside bill savings – is reshaping the product mix that manufacturers must offer to compete effectively in India. For utility-scale projects, central inverters from Sungrow, Huawei, and TMEIC dominate the procurement landscape. India’s large solar parks in Rajasthan, Gujarat, and Andhra Pradesh specify central inverters in the 2.5 MW to 6.3 MW range – the most cost-effective configuration for projects above 50 MW.

China and India drive solar deployment at the highest levels of the worldwide market while operating from Asia-Pacific. The demand increase for clean energy sources will drive the PV inverter market towards substantial growth during upcoming years. Key inverter brands with significant Indian market presence include Sungrow, Huawei, GoodWe, Growatt, Solis, Delta Electronics, SMA, and domestic manufacturers including SONA, Havells, and Luminous – which primarily serve the residential off-grid and hybrid segments.

The Technology Trends Reshaping the Solar Inverter Industry Through 2030

AI-Driven Energy Management

The most significant technology trend across all inverter categories is the integration of artificial intelligence into energy management. Advanced technologies like artificial intelligence and the Internet of Things have improved inverter capabilities through real-time analysis and predictive maintenance while enhancing energy management capabilities.

Huawei’s AI-powered smart PV platform uses machine learning to continuously optimize MPPT tracking, predict yield based on weather forecasts, detect early-stage faults before they cause failures, and maximize self-consumption in hybrid systems – delivering measurable yield improvements over conventional inverter control logic.

EV Charging Integration

Smart functions of the monitoring system, the capability of grid stabilisation, and the inclusion of EV charging support in solar inverters add more value to solar inverters. These developments go beyond just enhancing a system’s qualities as they also contribute to reducing the price estimates linked with installation and maintenance, thus expanding the availability of solar energy to a broader market segment.

The home energy system – solar panels, hybrid inverter, battery storage, and EV charger – is increasingly specified as an integrated bundle rather than separate components. Manufacturers that can offer seamless integration across all four components hold a significant advantage over those offering only inverters in isolation.

Virtual Power Plant Readiness

In October 2025, the Solar Hybrid Inverters Market saw a major product launch with the introduction of new hybrid string inverters for residential and commercial applications, enabling advanced energy storage and reliable backup power solutions. Virtual power plant readiness – the ability for a residential or commercial inverter to participate in aggregated demand response or grid support programs – is moving from a premium feature to a standard specification requirement in markets like Australia, the UK, Germany, and increasingly India.

2,000-Volt Architecture

The implementation of 2,000-volt inverters shows potential to extend solar panel arrays while enabling substantial savings in balance-of-system spending. Higher system voltage reduces cable cross-section requirements, improves efficiency, and allows longer string lengths – all of which reduce the balance-of-system cost for utility-scale projects. Several major manufacturers including Sungrow and Huawei have launched 2,000V utility-scale inverter products that are now being specified in the largest solar park projects globally.

Cybersecurity Requirements

Developers, investors, and lenders place increasing emphasis on manufacturing diversification, cybersecurity readiness, and long-term operational reliability when selecting inverter suppliers. Timothy Shen of Wood Mackenzie said buyers are increasingly assessing manufacturers on their ability to provide reliable long-term support, maintain diversified manufacturing footprints, and meet growing cybersecurity and compliance requirements alongside traditional performance metrics.

For manufacturers with significant Chinese ownership – which includes several of the top-ranked global suppliers – cybersecurity scrutiny from Western governments and utilities is creating real commercial headwinds in certain markets, particularly the United States, Australia, and the United Kingdom. This geopolitical dimension of the inverter market is becoming as important as the technical dimension for many procurement decisions.

Localised Manufacturing

In an increasingly protectionist policy environment, localized production has become a key competitive factor. In February 2026, Sungrow announced plans to open its first factory in Europe to strengthen local manufacturing and service capabilities. In September 2025, SMA Solar partnered with Create Energy to manufacture Sunny High-power PEAK3 inverters at a Tennessee facility under USA domestic content incentives.

For India specifically, the government’s focus on domestic manufacturing through PLI and preferential procurement policies means that inverter manufacturers with Indian assembly or manufacturing facilities hold a structural competitive advantage in the government-supported segment of the market.

The Challenges Every Solar Inverter Company Faces

No honest market assessment ignores the genuine headwinds facing this industry. A major market restraint is component shortages that still slow down production, with more than 30% of installers reporting delays tied to power-electronics availability during recent procurement cycles. Power semiconductors – particularly silicon carbide and gallium nitride switches that underpin the efficiency gains in modern inverters – remain supply-constrained, limiting the production ramp that several manufacturers need to meet demand.

Pricing pressure is intense and worsening. Price pressures and workforce layoffs at Enphase Energy and SolarEdge Technologies are among the current challenges faced by the solar industry, as Chinese manufacturers continue to reduce prices in international markets where they are competing against established Western and Israeli brands.

Warranty and bankability concerns are rising as a new generation of lower-cost manufacturers enters the market. Lenders and insurers evaluating solar project finance now conduct increasingly rigorous assessments of inverter manufacturer financial stability and service network capability – favoring established Tier 1 brands and placing smaller or newer entrants at a significant disadvantage when projects need long-term debt financing.

What This Market Means Segment by Segment for Your Business

For residential solar installers in India: The PM Surya Ghar program has created unprecedented residential inverter demand. The shift toward hybrid inverters in new installations is the most commercially significant trend – installers who offer hybrid-ready systems as a standard option are seeing higher average project values and stronger customer satisfaction scores than those still selling string-only configurations.

For commercial and industrial solar buyers: The economics of hybrid inverters combined with BESS are compelling – reducing electricity costs through peak shaving, providing backup power during grid outages, and enabling participation in demand response programs. The total system cost is higher than string-only configurations, but the payback period is shorter when all revenue streams are included.

For utility-scale developers: Central inverter selection is increasingly about long-term bankability, service network strength, and cybersecurity compliance alongside traditional efficiency and cost metrics. Sungrow and Huawei dominate on pure technical merit; SMA and Fronius dominate in markets where European or Western supply chains are preferred.

For inverter manufacturers targeting India: The combination of PM Surya Ghar driving residential hybrid demand, utility-scale solar parks driving central inverter demand, and PLI incentives potentially rewarding domestic manufacturing creates a three-layer market opportunity that is genuinely unique to India right now.

Why World Green Energy & Sustainability (WGES) Expo 2027 Is the Platform Where Inverter Manufacturers Meet India’s Buyers

Every type of solar inverter manufacturer and buyer profiled in this article – from global giants like Sungrow and Huawei to regional specialists like Growatt and GoodWe, from residential rooftop installers seeking the best hybrid inverter for PM Surya Ghar projects to utility-scale developers specifying central inverters for gigawatt-scale solar parks – converges on one fundamental commercial need: face-to-face conversations with procurement decision-makers in the world’s fastest-growing solar market.

Gujarat, host state of World Green Energy & Sustainability (WGES) Expo 2027, is India’s rooftop solar capital – the state with more PM Surya Ghar installations than any other. It is also home to Adani Solar’s utility-scale procurement operation, Waaree Energies’ manufacturing headquarters, and direct access to the renewable energy development corridor that runs from Kutch to Rajasthan. Every type of inverter buyer operating in India is either headquartered in Gujarat or actively procuring for projects in and around Gujarat.

The criteria used to evaluate inverter suppliers continue to expand as solar projects become larger and more complex. Buyers are increasingly assessing manufacturers on their ability to provide reliable long-term support, maintain diversified manufacturing footprints, and meet growing cybersecurity and compliance requirements. These assessments happen in conversations – at technical conferences, exhibition stands, and one-to-one meetings where manufacturers demonstrate products, answer technical questions, and build the relationships that lead to long-term supply agreements.

World Green Energy & Sustainability (WGES) Expo 2027 is where those conversations happen, in the market that matters most, with the buyers that matter most. World Green Energy & Sustainability (WGES) Expo 2027 in Gandhinagar, Gujarat, is your fastest and most direct route to those relationships.

Register as an exhibitor at the World Green Energy & Sustainability (WGES) Expo 2027 today. Secure your position in front of India’s most active solar buyers, developers, investors, and policymakers – all in one place, at the moment the market is moving fastest.

For more details: contact us at info@adexexhibitions.com | +91 81770 53335 | +91 91528 96078

For Exhibitor Registration: If you have not registered, you may also fill out this Exhibitor Registration Form.