The Technology That Just Overtook a Century of Infrastructure

A genuinely historic threshold was crossed in the global energy storage industry in 2025 – one that received far less attention than it deserved.

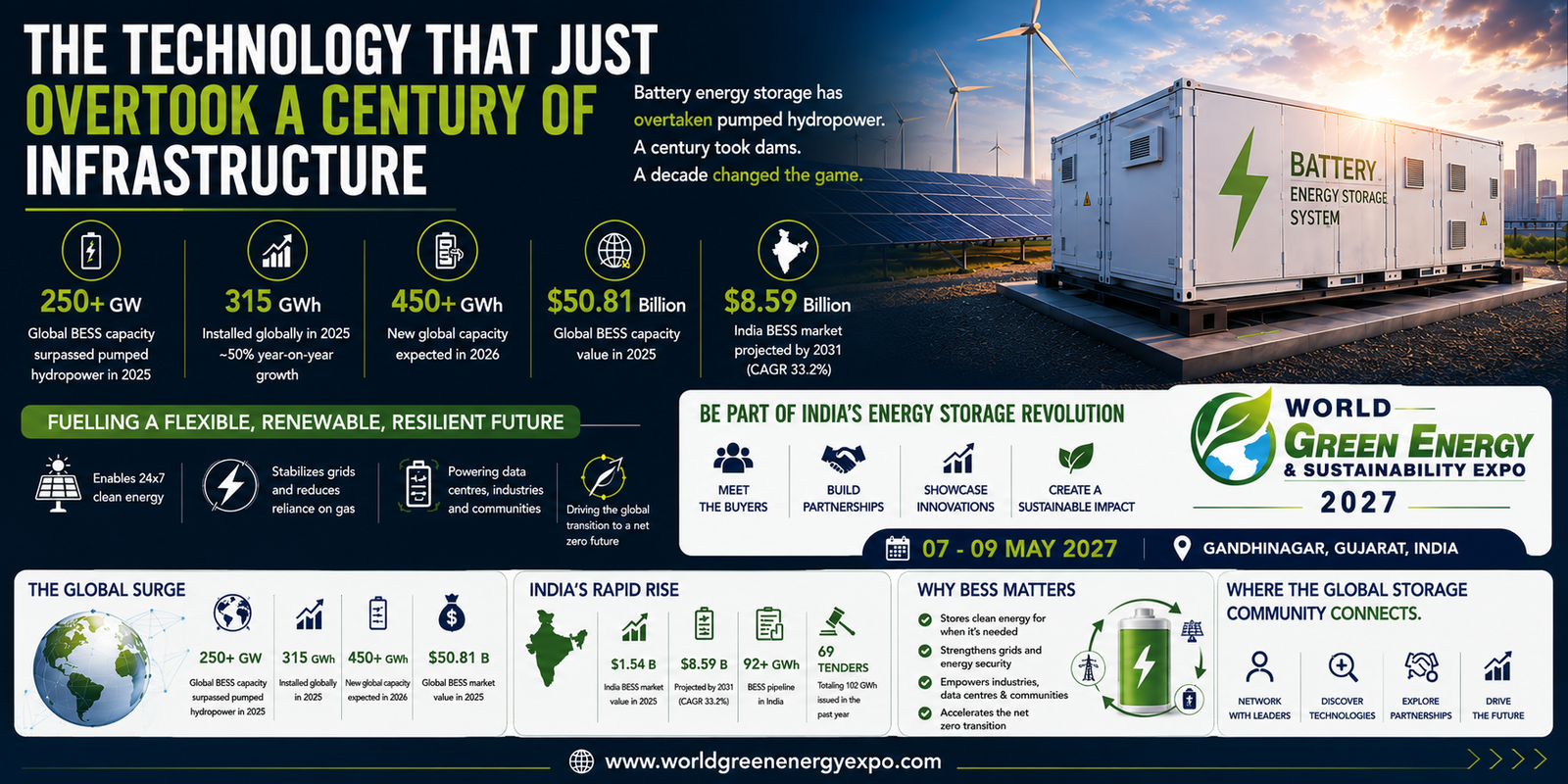

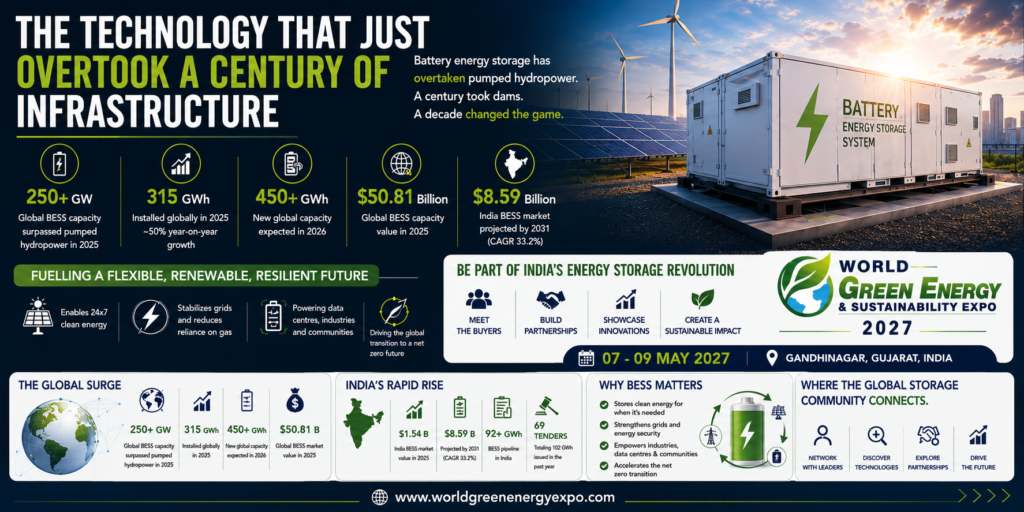

After a historic 2025, when global BESS capacity surpassed 250 GW and overtook pumped hydropower, momentum is set to accelerate further in 2026, with key markets expanding and battery storage increasingly replacing gas generation. Pumped hydropower took nearly a century of dam-building, reservoir engineering, and civil infrastructure investment to reach its current global scale. Battery energy storage systems overtook it in roughly a decade – a pace of infrastructure deployment with almost no historical precedent in the energy sector.

Around 315 GWh of battery energy storage was installed globally across both grid-scale and behind-the-meter markets in 2025, representing nearly 50% year-on-year growth, according to Benchmark Mineral Intelligence. Looking ahead, 2026 is forecast to see new operational capacity exceed 450 GWh, with no material supply constraints expected as cell production continues to outpace demand growth.

For battery cell manufacturers, system integrators, power electronics companies, fire safety specialists, and grid technology providers worldwide, 2027 represents the moment this market shifts from rapid growth to full-scale industrial maturity. This article brings together the complete global and India-specific picture – market size, technology, leading companies, and country policy – that every BESS industry professional needs heading into the year ahead.

Global Market Size and Growth – The Numbers That Define BESS in 2027

The scale of expansion in battery storage over the past two years is best understood through shipment volumes rather than valuation alone, since methodologies for market sizing vary widely across research houses.

Global shipments of battery energy storage systems increased by 75.5%, reaching 421.2 GWh in 2025, with 600 GWh projected for 2026, according to InfoLink Consulting. Global shipments of the underlying energy storage cells reached 612.39 GWh in 2025, nearly doubling from the previous year, with the 2026 forecast standing at 801 GWh.

Grid-scale projects were the primary driver of this growth, accounting for nearly 240 GWh of global installations in 2025. Project sizes continued to increase, with 46 giga-scale projects entering operation during the year, up sharply from just 17 in 2024. More than 150 giga-scale projects are currently in the pipeline for 2026.

On market valuation, estimates vary considerably depending on scope, but the direction is consistent across every major research house. One widely cited estimate places the global BESS market at USD 50.81 billion in 2025, projected to reach USD 105.96 billion by 2030 at a CAGR of 15.8%, driven by rapid renewable energy deployment, grid modernization initiatives, and the rising need for peak load management and frequency regulation.

By region, Asia-Pacific held 49.85% of the battery energy storage system market share in 2025, while the Middle East and Africa region is projected to expand at the fastest CAGR of 19.07% through 2031.

A significant new demand driver has entered the picture over the past year. As AI-based data centres consume an increasing share of grid capacity, the role of on-site energy storage is expanding beyond providing uninterruptible power supply, with battery systems deployed alongside data centres increasingly capable of supporting grid frequency regulation. This is creating an entirely new category of BESS buyer – hyperscale technology companies – alongside the traditional utility and renewable developer customer base.

Where in the World Is BESS Being Deployed

China and the United States led global BESS deployments in 2025, with China far outpacing all other markets – the world’s largest BESS market installed more battery capacity in December alone than the United States, the second-largest market, deployed over the entire year.

The rest of the global top five has shifted meaningfully. Saudi Arabia, Australia, and Chile moved into third, fourth, and fifth place respectively in 2025, displacing the United Kingdom and Italy from the previous year’s top five markets. This reshuffling reflects how quickly countries with strong solar resources and limited grid infrastructure are using BESS to leapfrog directly into flexible, renewables-heavy power systems.

Europe installed 25.3 GWh of new storage capacity in 2025 and is set to add 35.1 GWh in 2026. With 27.1 GWh installed in 2025, battery storage achieved its twelfth consecutive year of record growth in the European Union. However, the EU would need a tenfold increase in current annual deployment, bringing battery storage to 750 GWh over the next five years, to meet its own stated targets – meaning current growth, while encouraging, remains insufficient against policy goals.

India’s BESS Market – The Fastest-Growing Storage Opportunity in Asia

India’s battery storage sector has moved from a near standing start to one of the most closely watched markets in the world within the space of about eighteen months.

The India Battery Energy Storage System Market was valued at USD 1.54 billion in 2025 and is estimated to grow from USD 2.05 billion in 2026 to reach USD 8.59 billion by 2031, at a CAGR of 33.2%. Other research houses place the broader energy storage systems market – including non-BESS technologies – considerably higher. The India Energy Storage Systems Market is projected to be valued at USD 3.7 billion in 2026, with the electrochemical BESS segment expected to account for approximately 40% of the market by technology, growing at a CAGR of 28.7% from 2026 to 2033. The pipeline behind these figures is substantial. A whitepaper cited by PV Magazine India notes that cumulative installed stationary BESS in the country is still under 1 GWh today, but the project pipeline already exceeds 92 GWh, with 69 new BESS tenders totalling 102 GWh issued over the past year alone.

The Central Electricity Authority projects a 47 GW storage need by 2030, yet installed grid-scale capacity was under 1 GW in early 2024, prompting utilities to accelerate procurement through multi-hour standalone tenders. The National Electricity Plan targets approximately 47 GW and 236 GWh of storage capacity by 2032.

India’s project landscape is already producing landmark installations. In November 2025, Adani Group announced its entry into India’s BESS market with a 1,126 MW / 3,530 MWh project at Khavda, Gujarat, slated for commissioning by March 2026. The deployment of over 700 lithium-ion BESS containers will make it the largest single-location BESS in India and among the world’s largest.

Adani Energy Solutions commissioned a 40 MW/120 MWh BESS in Gujarat paired with 300 MW of solar under a 25-year PPA at INR 5.95 per kWh in October 2024, while Tata Power commissioned a 100 MW/200 MWh standalone project in Rajasthan at INR 5.85 per kWh under a similar 25-year structure in August 2024. NTPC’s Ramagundam integrated solar and battery project, at 33 MW/132 MWh, stands as the nation’s biggest grid-scale BESS as of mid-2025, while Amara Raja’s landmark 1,000 MWh standalone project in Rajasthan represents India’s largest battery storage installation and one of the few at gigawatt-hour scale globally.

Innovation in chemistry is also taking root domestically. Reliance New Energy energised a 5 MW/50 MWh vanadium flow battery in Gujarat in September 2024, marking the country’s first utility-scale non-lithium long-duration energy storage system.

India’s BESS Policy Framework – What Every Company Must Know

India’s central government has built a comprehensive policy architecture specifically designed to accelerate battery storage deployment.

Policy support includes a Production Linked Incentive (PLI) pool of INR 18,100 crore for domestic cells, a Viability Gap Funding grant covering up to 40% of standalone BESS capex, and rising Energy Storage Obligations that compel DISCOMs to source a share of their supply from storage-backed contracts. The Energy Storage Obligation, set at 1% in FY24 and scaling to 4% by FY30, along with Viability Gap Funding support of up to 40% of capital cost, has institutionalized long-term demand visibility for BESS deployment. Separately, MNRE’s mandate requires battery storage to be included in new solar and wind projects starting at 10% of plant capacity.

In June 2025, India’s Ministry of Power approved a Viability Gap Funding scheme for 30 GWh of BESS projects, in addition to 13.2 GWh already underway. On manufacturing, the 50 GWh Advanced Chemistry Cell PLI scheme is accelerating domestic battery manufacturing and supply chain localisation, directly targeting India’s historical dependence on imported battery cells.

For international companies, the cost-competitiveness this policy framework has unlocked is striking. India’s first commercially approved standalone BESS project at BRPL’s Kilokari substation, at 20 MW/40 MWh, set a levelized capacity tariff approximately 55% below previous benchmarks – confirming that BESS economics in India have crossed a critical inflection point.

India’s Leading BESS Companies – Manufacturers, Integrators and Developers

India’s BESS supply chain spans manufacturers, EPC integrators, and major renewable developers expanding into storage. The largest battery energy storage system companies in India by revenue include Exide Industries, Waaree Energies, Amara Raja Energy & Mobility, Sterling and Wilson Renewable Energy, and Luminous Power Technologies.

Waaree Energies

Waaree Energies has emerged as one of the most ambitious domestic manufacturers in the sector. Waaree’s Board of Directors approved an increase in the production capacity of its upcoming lithium-ion advanced chemistry storage cell and BESS manufacturing facility from 3.5 GWh to 20 GWh, with an additional capital expenditure of INR 8,000 crore. In February 2026, Waaree Energies unveiled plans to build a 16 GWh integrated lithium-ion battery gigafactory in Andhra Pradesh, investing approximately INR 8,175 crore, covering the full battery value chain including cells, packs, and large-scale BESS. Through product lines including the LIGER, LION, and LIT series under its Waaree Li-ion Batteries brand, the company delivers high energy density and versatile installation options spanning small-scale systems to larger grid applications.

Amara Raja Energy & Mobility

Amara Raja Energy & Mobility stands as India’s largest manufacturer of automotive batteries and allied products, closely following Exide in advanced chemistries and large-scale BESS integration, with in-house manufacturing capabilities enabling custom container and prefab solutions optimized through advanced CFD and thermal management. Amara Raja’s 16 GWh cell facility in Telangana is expected to begin production in 2027. The company signed a licensing agreement with Gotion-InoBat-Batteries, a unit of China’s Gotion High Tech, for lithium-ion LFP cell technology to set up gigafactory facilities in India.

Exide Batteries

Exide Industries remains the technology and market leader in battery technology, spanning lead-acid and pioneering lithium-ion manufacturing. Exide invested USD 120 million in its lithium-ion business in FY25 and plans a further USD 48 million in FY26 as part of a dual-focus growth strategy spanning lead-acid and lithium-ion technology.

JSW Energy

JSW Energy has moved decisively into storage as an extension of its renewable development portfolio. JSW Energy and Fluence formed a joint venture in September 2024 to deploy 500 MWh across Karnataka and Maharashtra by 2026, with a USD 150 million investment.

Beyond these domestic leaders, large Indian conglomerates including Tata Power Solar, Mahindra Susten, Adani Green Energy, and ReNew Power offer integrated BESS solutions using imported cells, competing on project scale, EPC capability, and balance sheet strength. Specialized providers such as Fluence, Sungrow Power Supply, and Delta Electronics supply modular BESS systems through Indian subsidiaries or channel partners, competing on technology, efficiency, and warranty terms.

Utility-scale tenders in India are dominated by a small group of large players – Tata Power, Adani, Fluence, and Sungrow – due to capital requirements and project execution track record, while the commercial and industrial segment is far more fragmented, with over 50 active system integrators and pack providers competing on price, service coverage, and warranty terms.

The Global Technology Leaders Shaping the BESS Industry

Beyond India, a small number of global companies dominate worldwide BESS deployment, split between cell manufacturers and system integrators.

CATL commands over 36% of the global battery market share and is the primary technology provider for nearly every major integrator, including Tesla, Fluence, and Sungrow, while simultaneously deploying its own branded systems.

According to Benchmark’s Battery Energy Stationary Storage Service, BYD shipped over 60 GWh of energy storage systems globally in 2025, ranking first among all BESS system integrators worldwide. Tesla deployed 46.7 GWh during the same period – a 49% year-over-year increase that was still not enough to keep pace with BYD’s expansion. Sungrow claimed third spot with 9% market share, followed by CRRC Zhuzhou, CATL, and Hyper Strong tied at 6% each, with Huawei, Envision, Fluence, and Sunwoda rounding out the top ten. Eight of the top ten BESS system integrators globally are Chinese companies, with Fluence – a joint venture between Siemens and AES – standing as the only Western company besides Tesla to crack the top tier.

Sungrow reported a 105% revenue increase in its energy storage division in 2025, surpassing 50 GW of shipments in key markets including India, with its ability to seamlessly integrate its own inverters with battery storage making it a preferred one-stop-shop supplier for utility-scale developers worldwide.

LG Energy Solution shifted strategy in 2025 to challenge Chinese dominance by commencing mass production of lithium iron phosphate batteries at its facilities in the United States, repurposing significant manufacturing capacity in Michigan to serve the stationary storage market.

Founded in 2018 by Siemens and AES, Fluence operates in 47 markets with over 225 projects delivered, with its digital optimization platform Fluence IQ widely used to enhance the real-world performance of renewable and storage assets.

Technology Trends Defining BESS Through 2030

Lithium iron phosphate was the fastest-growing battery chemistry in 2025, with demand rising 48% year-on-year, driven by the rapid expansion of the global BESS market. Outside China, LFP’s share of battery demand also increased to more than 30%, while the overall share of nickel-based chemistries declined. In India specifically, lithium-ion technologies led by LFP made up 92.15% of installed BESS capacity in 2025.

Sodium-ion technology is emerging as the next major chemistry shift. CATL is targeting mass production of its Naxtra sodium-ion line by December 2025, aiming for 175 Wh per kilogram energy density and 40 GWh of annual capacity, while Faradion – now owned by Reliance Industries of India – is building a 30 GWh sodium-ion gigafactory scheduled for completion around the end of 2025.

Long-duration storage remains a significant frontier still being solved. Long-duration systems accounted for only 6% of global energy storage installations in 2025, as shorter-duration lithium-ion batteries continue to dominate deployment.

Costs continue their steep decline. Lithium iron phosphate cell prices fell to USD 89 per kWh in Q2 2024, 14% below the 2023 level, after Chinese gigafactories ramped up output and cathode chemistries improved. The drop cut the capex of a 100 MWh utility project from USD 40 million in 2022 to about USD 30 million in 2024, pushing levelized storage costs below INR 5 per kWh in high-utilization nodes.

Safety regulation is tightening globally following high-profile incidents. US jurisdictions now require full-scale thermal-runaway testing, dedicated fire suppression, and wider separation distances. While compliance inflates balance-of-plant costs and lengthens permitting in space-constrained sites, stricter codes are bolstering insurer confidence and paving the way for wider institutional adoption.

Challenges the Industry Must Still Solve

Despite the extraordinary growth trajectory, several structural challenges remain across both the global and Indian BESS markets.

Skilled workforce gaps in system design, commissioning, and operations and maintenance for BESS are widely reported in India, with fewer than 500 certified system integrators nationwide capable of handling utility-scale installations as of 2025. Safety certification infrastructure is also underdeveloped, with testing and certification for UL 9540 and IEC 62619 equivalents taking 6 to 9 months, creating bottlenecks for new entrants and imported system components.

Pricing pressure is intensifying competition industry-wide. System prices have fallen 30 to 40% since 2023, compressing margins for integrators and driving consolidation among smaller players. In 2025, BESS system pricing reached new lows, with project tenders in China falling to as low as USD 63 per kilowatt-hour, and this aggressive pricing has filtered into export markets as integrators look toward higher-margin regions.

In India specifically, early-year growth from 2024 to 2026 remains modest owing to EPC lead times, regulatory approvals, and supply-chain constraints, with the accelerating slope of the deployment forecast curve from 2026 onward reflecting the expected commissioning of awarded large-scale BESS tenders and rapid scale-up of domestic manufacturing under the PLI-ACC program.

What This Means for World Green Energy & Sustainability (WGES) 2027 Exhibitors and Visitors

The data points to an unambiguous conclusion: battery energy storage has moved from emerging technology to essential infrastructure, and the procurement decisions being made right now – by Indian developers, global integrators, and government agencies alike – will shape the supply chains and partnerships of the next decade.

For battery cell manufacturers, system integrators, power conversion system suppliers, thermal management and fire safety specialists, and energy management software providers, the opportunity in India alone spans a project pipeline already exceeding 92 GWh, with 69 new BESS tenders totalling 102 GWh issued in the past year alone.

World Green Energy & Sustainability (WGES) Expo 2027 brings together exactly the audience this rapidly scaling industry needs to reach: India’s leading developers including Adani Green Energy, Tata Power, JSW Energy, and Waaree Energies who are actively procuring storage technology; EPC contractors and system integrators evaluating new suppliers; government and utility representatives shaping India’s storage policy; and international investors assessing where global capital should flow next in the energy storage value chain.

Gujarat – the host state of World Green Energy & Sustainability (WGES) Expo 2027 is itself central to this story, anchored by Adani Green Energy’s 1,126 MW Khavda BESS project, Reliance New Energy’s pioneering vanadium flow battery installation, and the broader wave of solar-plus-storage tendering happening across the state’s renewable energy corridor.

Whether you manufacture battery cells, integrate complete storage systems, supply power electronics and safety technology, or provide the software platforms that optimize storage performance – World Green Energy & Sustainability (WGES) Expo 2027 is where India’s storage industry is building its next chapter.

Register as an exhibitor at the World Green Energy & Sustainability (WGES) Expo 2027 today. Secure your position in front of India’s most active BESS buyers, developers, investors, and policymakers – all in one place, at the moment the market is moving fastest.

For more details: contact us at info@adexexhibitions.com | +91 81770 53335 | +91 91528 96078

For Exhibitor Registration: If you have not registered, you may also fill out this Exhibitor Registration Form.