India Has Crossed a Historic Milestone – And the Race Is Just Beginning

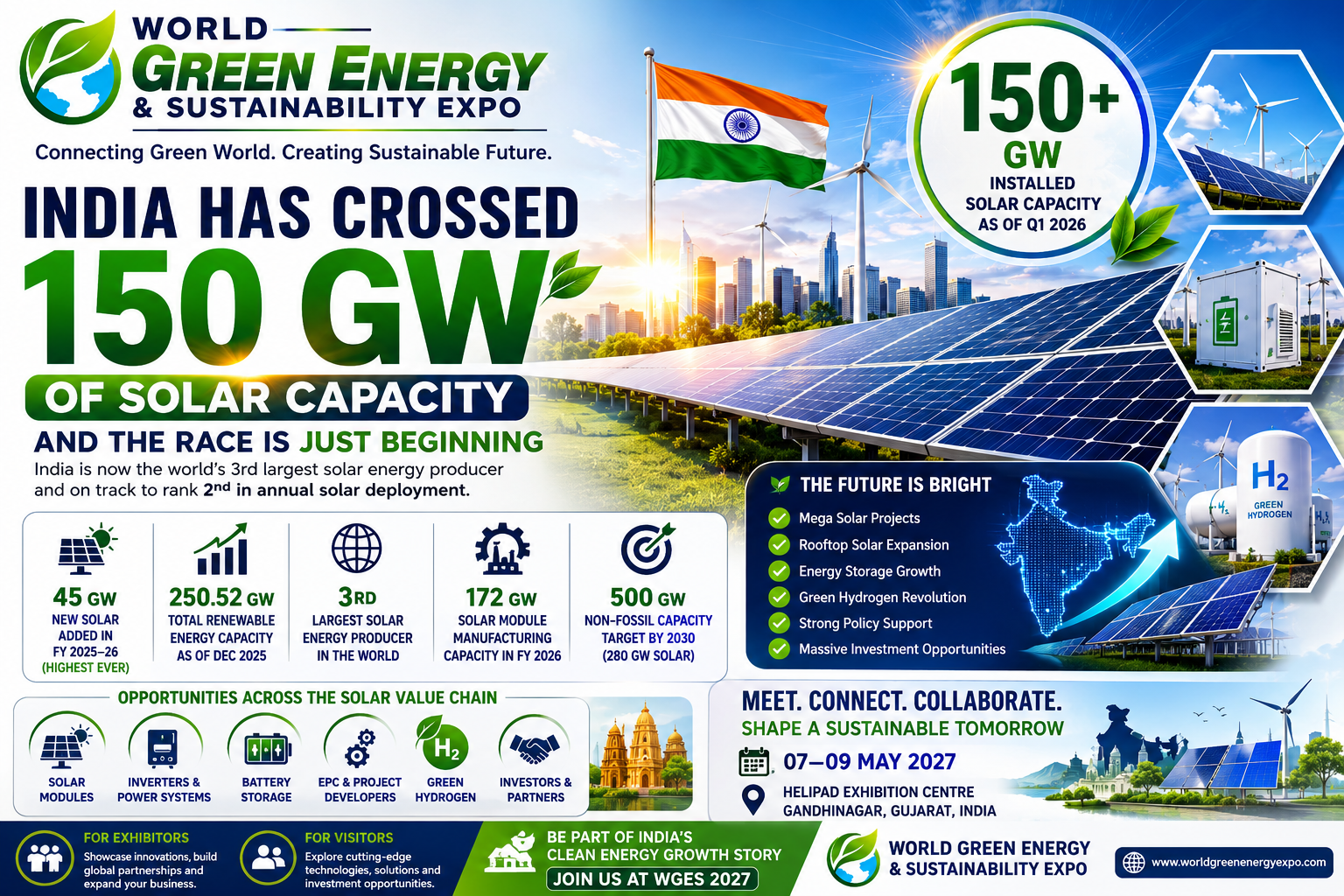

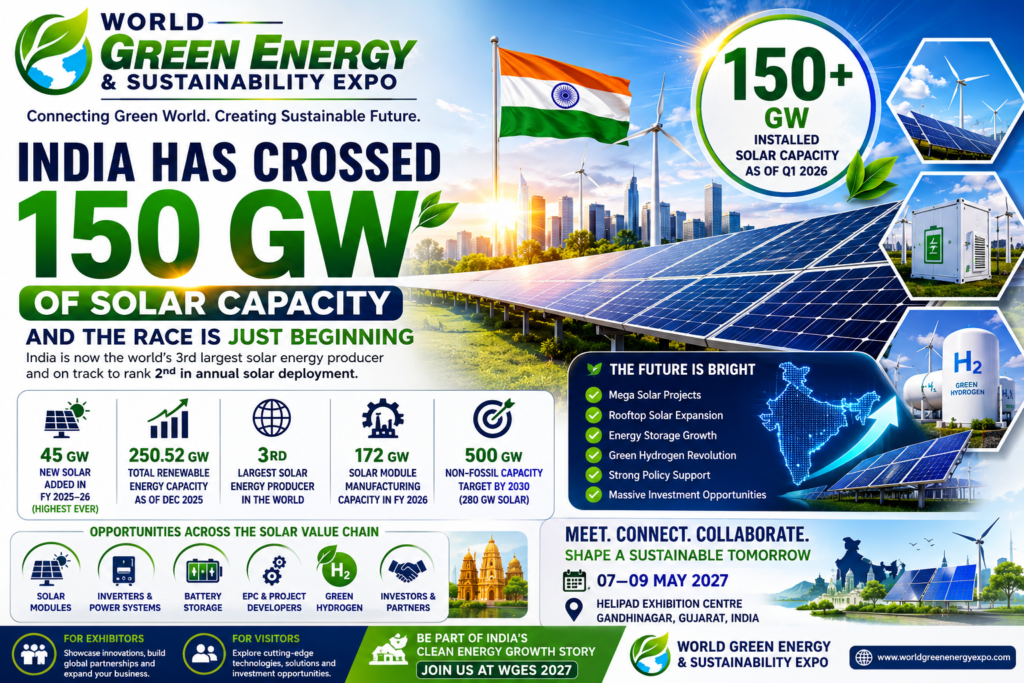

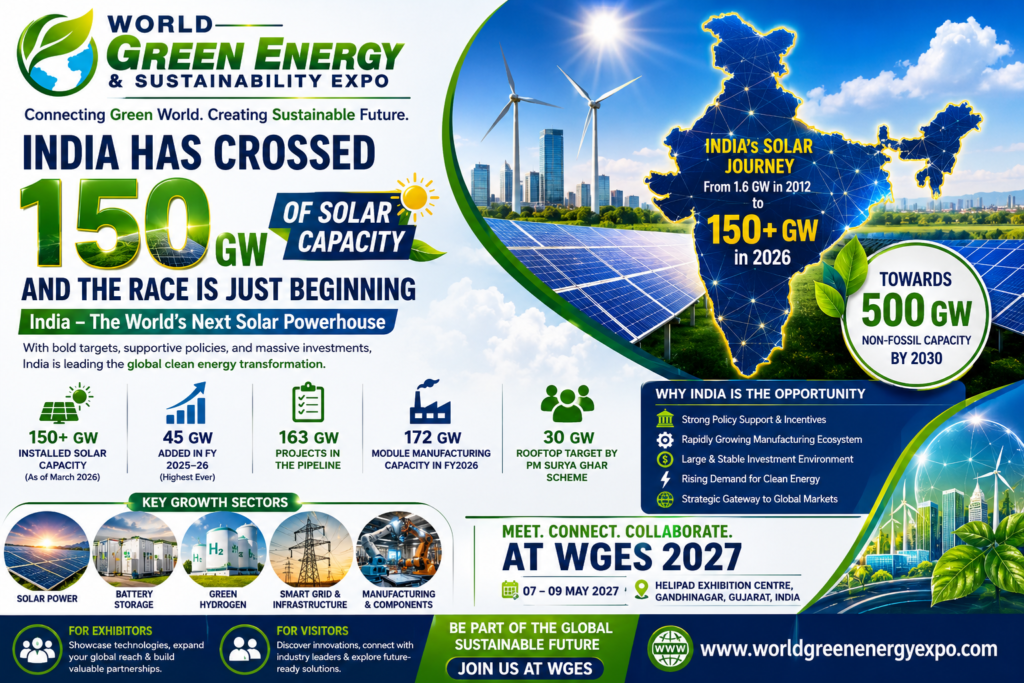

On March 31, 2026, India crossed 150 gigawatts of installed solar capacity – a number that would have seemed impossible a decade ago, and one that has fundamentally repositioned the country in the global energy order.

India crossed 150 GW of installed solar capacity at the end of Q1 2026, overtaking the United States to become the world’s third-largest solar producer. In the same financial year, India recorded a solar energy capacity addition of around 45 GW in 2025–26 – its highest ever in a single year – a figure that outpaces most countries entire installed solar base.

India ranked 3rd globally in renewable energy installed capacity, reaching 250.52 GW as of December 2025, according to IRENA Renewable Energy Statistics 2026. More significantly, India has officially surpassed Japan to become the world’s third-largest solar energy producer, generating 1,08,494 GWh of solar power, exceeding Japan’s 96,459 GWh.

But here is what makes 2027 truly significant: India is not slowing down. It is accelerating. With 42.5 GW expected in new installations through 2026 alone, the country is now on a trajectory to rank second globally in annual solar deployment – behind only China.

For solar panel manufacturers, EPC contractors, inverter companies, battery storage providers, rooftop solar installers, and clean energy investors worldwide, India in 2027 is not just an opportunity – it is the single most important solar market on earth outside China.

Market Size and Growth – The Numbers That Define India’s Solar Story

India’s solar energy journey from 1.6 GW in 2012 to 150 GW in 2026 is one of the fastest capacity expansions in the history of any energy technology in any country. Solar photovoltaic accounted for 99.58% of the India solar energy market in 2025 and is on track for a 19.08% CAGR through 2031.

The scale of what is being built is staggering. As of 2025, 163 GW of large-scale solar projects sit in various development stages, giving investors line-of-sight on offtake and policy stability. This pipeline alone – before any new tenders are announced – represents more solar capacity than most countries have ever installed in total.

India’s renewable energy sector overall is growing at an extraordinary pace. Power generation from renewable energy sources stood at 283.62 billion units during April 2025 to February 2026, increasing from 230.87 BU in the same period of the previous year, reflecting a strong year-on-year growth of 22.85%.

On the manufacturing side, India is building a formidable domestic industry. India’s module manufacturing capacity reached 172 GW in FY2026, with cell capacity being ramped rapidly, with targets exceeding 90 GW by Q1 FY2027. Within PV, TOPCon modules already form 35% of domestic output after Waaree, Adani, and Premier ramped 18 GW combined capacity.

The financial commitment from government to support all this growth is enormous. India’s total installed power capacity reached 520.51 GW as of January 2026, with solar leading all categories in new additions. The Union Budget 2026–27 significantly strengthens India’s renewable energy push, with the Ministry of New and Renewable Energy allocation reaching record levels.

India’s National Solar Energy Target – 500 GW by 2030 and What It Means for Business

Every number in India’s solar energy story flows from one overarching commitment: India’s commitment to achieving 500 GW of non-fossil fuel-based capacity by 2030, with solar power expected to contribute a substantial portion, aiming for 280 GW of solar PV capacity by that year.

To understand the scale of this ambition, consider where India stands today versus where it needs to be. With 150 GW installed as of March 2026, India needs to nearly double its installed solar energy base in four years. That means commissioning an average of 32 to 40 GW of new solar capacity every single year through 2030 – which is exactly what the current pipeline suggests.

NEP14 projects solar’s share in India’s power generation mix climbing from 5% in FY 2022 to 17% in FY 2027, and ultimately reaching 25% by 2032. For context, solar currently meets approximately 8% of India’s electricity demand – the scale of the expansion ahead is immense.

The NEP14 targets also include storage capacity that will be capable of shifting 6% and 15% of renewable energy generation to non-solar hours by FY 2027 and FY 2032, respectively, creating a massive parallel opportunity in battery energy storage systems alongside solar deployment.

For businesses planning market entry or expansion in India, this national target is the single most important policy signal. It means the Indian government is structurally committed to buying, building, and supporting solar at enormous scale for the rest of this decade. The tender pipeline, the subsidy structures, the import duties, and the grid upgrade investments all flow from this target. Companies that position now – through exhibition at industry events, distribution partnerships, and technology licensing – will be best placed to capture the contracts that will flow from it.

India’s Key Solar Policies – What Every Company Must Know in 2027

India’s solar energy market is shaped by a set of powerful government policy frameworks. Understanding these is essential for any company seeking to do business in the Indian solar sector.

PM Surya Ghar: Muft Bijli Yojana – The Rooftop Solar Revolution

The single most transformative new policy for the Indian solar sector is PM Surya Ghar: Muft Bijli Yojana, launched in February 2024. With a financial outlay of INR 75,021 crore (USD 8.53 billion), the scheme targets 30 gigawatts of residential rooftop solar capacity and coverage of 10 million households by FY2027.

The scheme provides direct subsidies to homeowners of up to INR 78,000 per household for rooftop solar installation, making solar genuinely affordable for India’s growing middle class for the first time. The results have been immediate. As of March 2026, 26.19 lakh systems had been installed, with the scheme disbursing Rs. 17,967.53 crore (USD 2.03 billion) as Central Financial Assistance, supported by a fully digital subsidy mechanism with an average processing time of around 15 days.

Gujarat leads all states with the highest installed residential rooftop solar capacity of 1,491 MW under PM Surya Ghar, followed by Maharashtra, Uttar Pradesh, Kerala, and Rajasthan. These five states together account for approximately 77.2% of total installed capacity under the scheme.

For rooftop solar installers, system integrators, inverter manufacturers, mounting structure providers, and EPC companies, PM Surya Ghar represents one of the largest government-funded demand creation programs for residential solar anywhere in the world. The 5.8 million applications already filed represent a pipeline of potential installations that will keep the sector busy for years.

Production Linked Incentive (PLI) Scheme – Building India’s Solar Manufacturing Base

India is not content to merely install solar – it wants to manufacture it. The PLI scheme for high-efficiency solar PV modules is transforming India from an importer into a global producer. India’s PLI scheme has led to 18.5 GW of module capacity, 9.7 GW of solar cell capacity, and 2.2 GW of ingot-wafer capacity being established as of June 30, 2025. The program has awarded a total of 48 GW of module manufacturing capacity.

The PLI scheme has attracted INR 52,900 crore in investment as of September 2025, boosting domestic solar PV manufacturing capacity at scale.

The ALMM (Approved List of Models and Manufacturers) policy reinforces this manufacturing drive. From June 1, 2026, any net-metering project or open-access renewable energy project commissioned on or after that date must use ALMM-listed, locally made panels and cells. This effectively mandates Indian-manufactured solar modules for all domestic solar projects, creating a guaranteed domestic market for Indian and India-based manufacturers.

For international solar manufacturers, this policy creates both a challenge and an opportunity. The challenge is that imported panels face significant headwinds in the Indian market. The opportunity is that establishing manufacturing in India – through joint ventures, technology licensing, or wholly owned facilities – gives access to both the Indian domestic market and India’s growing solar export ambitions.

PM KUSUM – Solarising Indian Agriculture

PM KUSUM is transforming Indian agriculture by replacing diesel-powered irrigation pumps with solar-powered alternatives. The PM KUSUM scheme has already solarised over 10 lakh farm pumps, reducing diesel use in agriculture. The scheme targets 35 GW of solar capacity across agricultural applications.

For solar pump manufacturers, rural electrification companies, and agricultural equipment suppliers, PM KUSUM represents a multi-billion dollar market opportunity spread across India’s vast agricultural hinterland.

State-by-State Solar Landscape – Where the Opportunities Are

India’s solar market is not uniform across its 28 states. Understanding the state-level landscape is critical for targeting your business development efforts.

Rajasthan and Gujarat are the undisputed leaders in utility-scale solar, accounting for the largest share of large-scale project installations. States like Rajasthan and Gujarat led in large-scale installations, accounting for 38% and 35% of capacity additions respectively during India’s record-breaking quarter of solar additions in early 2024. Both states have vast land availability, high solar irradiance, and strong state government support for renewable energy.

Gujarat holds a special significance. It is home to several of India’s most ambitious solar parks, leads the country in rooftop solar under PM Surya Ghar, and hosts Gandhinagar – the city of World Green Energy & Sustainability (WGES) Expo 2027 – which has positioned itself as India’s clean energy capital with direct access to the country’s largest solar manufacturing base.

Tamil Nadu and Karnataka lead in commercial and industrial (C&I) rooftop solar, where large manufacturing facilities, IT campuses, and commercial buildings are installing solar at scale to reduce electricity costs and meet corporate sustainability targets.

Maharashtra, Uttar Pradesh, and Andhra Pradesh are rapidly growing markets with large industrial bases and strong government support for solar development.

For international companies visiting World Green Energy & Sustainability (WGES) Expo 2027, Gujarat and Rajasthan represent the immediate large-scale project opportunity, while the southern states represent the C&I and rooftop opportunity. Both are enormous.

Solar Manufacturing in India – The USD 172 GW Opportunity

India’s solar manufacturing sector has undergone a transformation as dramatic as its deployment story. India’s module manufacturing capacity reached 172 GW in FY2026, making it one of the largest solar manufacturing bases in the world after China.

The leading Indian solar manufacturers – Waaree Energies, Adani Solar, Tata Power Solar, Vikram Solar, and Goldi Solar – have all significantly expanded capacity and are now competing in global export markets. Tata Power, Waaree Energies, and Goldi Solar commissioned large plants in 2025, keeping domestic module margins in the 12–14% range despite import duties.

Adani Group plans to build 10 GW of solar manufacturing capacity by 2027, expanding its solar manufacturing business to meet growing demand in India and globally. Adani Solar has secured over 3,000 MW in exports and raised USD 394 million in financing from Barclays PLC and Deutsche Bank for solar manufacturing.

Technology is upgrading rapidly. TOPCon modules already form 35% of domestic output, while Reliance’s planned 10 GW HJT line targets 25-26% cell efficiency by 2027.

For equipment suppliers to solar manufacturing – glass, EVA, backsheet, frames, junction boxes, cell processing equipment, and automation systems – India’s manufacturing scale-up represents a direct and immediate procurement opportunity. These companies are exactly the type of exhibitor World Green Energy & Sustainability (WGES) Expo 2027 is designed to serve.

Foreign Direct Investment in Indian Solar Energy – Who Is Investing and How Much

India’s solar energy sector has attracted extraordinary foreign investment over the past five years, and the pipeline shows no signs of slowing.

Reliance Industries signed a pact with the Gujarat government to invest USD 80.61 billion in Gujarat over ten to fifteen years to set up 100 GW of renewable energy power plants and a green hydrogen ecosystem. This single commitment represents the largest private clean energy investment in Indian history.

International energy companies, private equity funds, infrastructure investors, and sovereign wealth funds from Japan, South Korea, the UAE, the USA, France, Germany, and Singapore have all made significant commitments to Indian solar projects over the past three years. The combination of India’s scale, its growing domestic manufacturing base, its 300-plus days of annual sunshine, its young and growing electricity demand, and its clear government policy framework makes it one of the most compelling solar investment destinations in the world.

For companies looking to enter the Indian market through joint ventures, technology partnerships, equipment supply agreements, or project co-development, the current moment is optimal. The market is large enough to absorb significant new entrants but not yet so consolidated that opportunities are closed.

Challenges and How the Industry Is Solving Them

No market of this scale and ambition is without challenges, and honesty about them is essential for companies making business decisions.

Grid and transmission constraints are the most immediate bottleneck. Solar penetration in leading states now exceeds 25% of peak demand, exposing grids to frequent curtailment events. India needs massive investment in grid upgrades, transmission lines, and energy storage to absorb the solar it is generating. This is simultaneously a challenge for solar developers and an enormous opportunity for grid technology companies, battery storage providers, and smart energy management solution providers.

Land acquisition remains complex. Large utility-scale solar projects require significant land parcels, and the acquisition process involves multiple government agencies with varying timelines. States with well-established solar parks – like Rajasthan’s Bhadla Solar Park and Gujarat’s Dholera Solar Park – help address this by providing pre-acquired, infrastructure-ready land to project developers.

Domestic manufacturing is not yet fully self-sufficient. PLI execution has been uneven, with only 56% of targeted module capacity and 14% of polysilicon capacity achieved as of mid-2025, meaning the domestic supply chain is still partially dependent on imports. This creates ongoing opportunities for equipment suppliers and material manufacturers who can serve India’s manufacturing scale-up.

The rooftop solar subsidy conversion rate needs improvement. Just 22.7% of PM Surya Ghar applications have translated into completed installations, reflecting bottlenecks in financing, vendor capacity, and approvals. For companies with solutions in digital financing, installation services, and supply chain management, this gap is a direct business opportunity.

The Technology Frontier – What Will Define Indian Solar Energy in 2027 and Beyond

India’s solar energy market is not just growing – it is upgrading technically at the same time.

TOPCon and HJT cell technology are replacing standard PERC modules as the dominant product. Higher efficiency modules reduce the land area and balance-of-system costs required per megawatt, improving project economics and making solar viable in more locations. Every efficiency point gained in cell technology has direct commercial value in a market where land cost and transmission access are constraints.

Floating solar energy is emerging as a major growth segment. The 600 MW floating solar plant in Madhya Pradesh is set to be one of the largest in the world, and several state governments are developing floating solar on reservoirs and irrigation canals as a way to generate solar power without consuming agricultural or industrial land.

Agrivoltaics – combining solar panels with agricultural production on the same land – is attracting growing attention as a way to simultaneously generate clean energy and continue food production, addressing the land use tension that constrains solar expansion in densely populated states.

Battery energy storage co-located with solar is becoming standard practice in new large-scale projects, driven by grid operators requiring dispatchable renewable power. The NEP14 targets 8.7 GW of battery storage capacity by March 2027 and 47.2 GW by March 2032, creating a market for battery storage systems that is growing as fast as solar itself.

Green hydrogen produced from solar electricity is creating a new demand frontier. ReNew aims to produce 1 million tonnes of green hydrogen annually, powered by 25 GW of renewables, while NTPC and Adani target multi-GW electrolyser facilities synchronized with utility-scale solar. For solar companies, the hydrogen economy is not a separate market — it is an extension of the solar market, creating massive incremental demand for solar electricity generation.

Why WGES 2027 Is the Essential Platform for India’s Solar Energy Industry

The World Green Energy & Sustainability (WGES) Expo 2027, held in 07th May – 09th May at Helipad Exhibition Centre, Gandhinagar, Gujarat – the capital of Gujarat, India’s leading solar state – is perfectly positioned to serve every segment of the Indian and global solar value chain.

Whether you are a solar panel manufacturer looking for Indian distribution partners, an EPC company seeking project opportunities, an inverter or mounting structure supplier targeting Indian rooftop installers, a battery storage company positioning for co-located solar-storage projects, a foreign investor researching the Indian market, or an Indian manufacturer seeking export opportunities – World Green Energy & Sustainability (WGES) Expo 2027 is where your most important conversations will happen.

Gujarat’s position at the heart of India’s solar economy means that World Green Energy & Sustainability (WGES) Expo 2027 attracts the procurement decision-makers, project developers, government officials, and technology buyers who are actively spending on solar right now. No other platform in Asia brings together the full solar value chain – from module manufacturers and inverter suppliers to EPC contractors, financiers, and government policymakers – under one roof, in the market that matters most.

World Green Energy & Sustainability (WGES) Expo 2027 is not just an exhibition. It is the defining business event for anyone serious about the Indian and Asian solar energy market.

India’s Solar Story Is the Biggest Business Opportunity in Clean Energy Today

The data is unambiguous. India is the market with the fastest growth in renewable electricity, and by 2026, new capacity additions are expected to double. A country that added 45 GW of solar energy in a single year, that has 163 GW in its active development pipeline, that is investing USD 8.53 billion in rooftop solar subsidies alone, that has committed to 500 GW of renewable capacity by 2030, and that is building 172 GW of domestic module manufacturing capacity is not a market you can afford to watch from the sidelines.

The companies that will capture the largest share of this market are the ones building relationships, demonstrating products, and establishing partnerships right now – in 2026 and 2027 – before the procurement decisions for the next wave of projects are made.

World Green Energy & Sustainability (WGES) Expo 2027 in Gandhinagar, Gujarat, is your fastest and most direct route to those relationships.

Register as an exhibitor at the World Green Energy & Sustainability (WGES) Expo 2027 today. Secure your position in front of India’s most active solar buyers, developers, investors, and policymakers – all in one place, at the moment the market is moving fastest.

For more details: contact us at info@adexexhibitions.com | +91 81770 53335 | +91 91528 96078

For Exhibitor Registration: If you have not registered, you may also fill out this Exhibitor Registration Form.