India Just Doubled Its Rooftop Solar in a Single Year

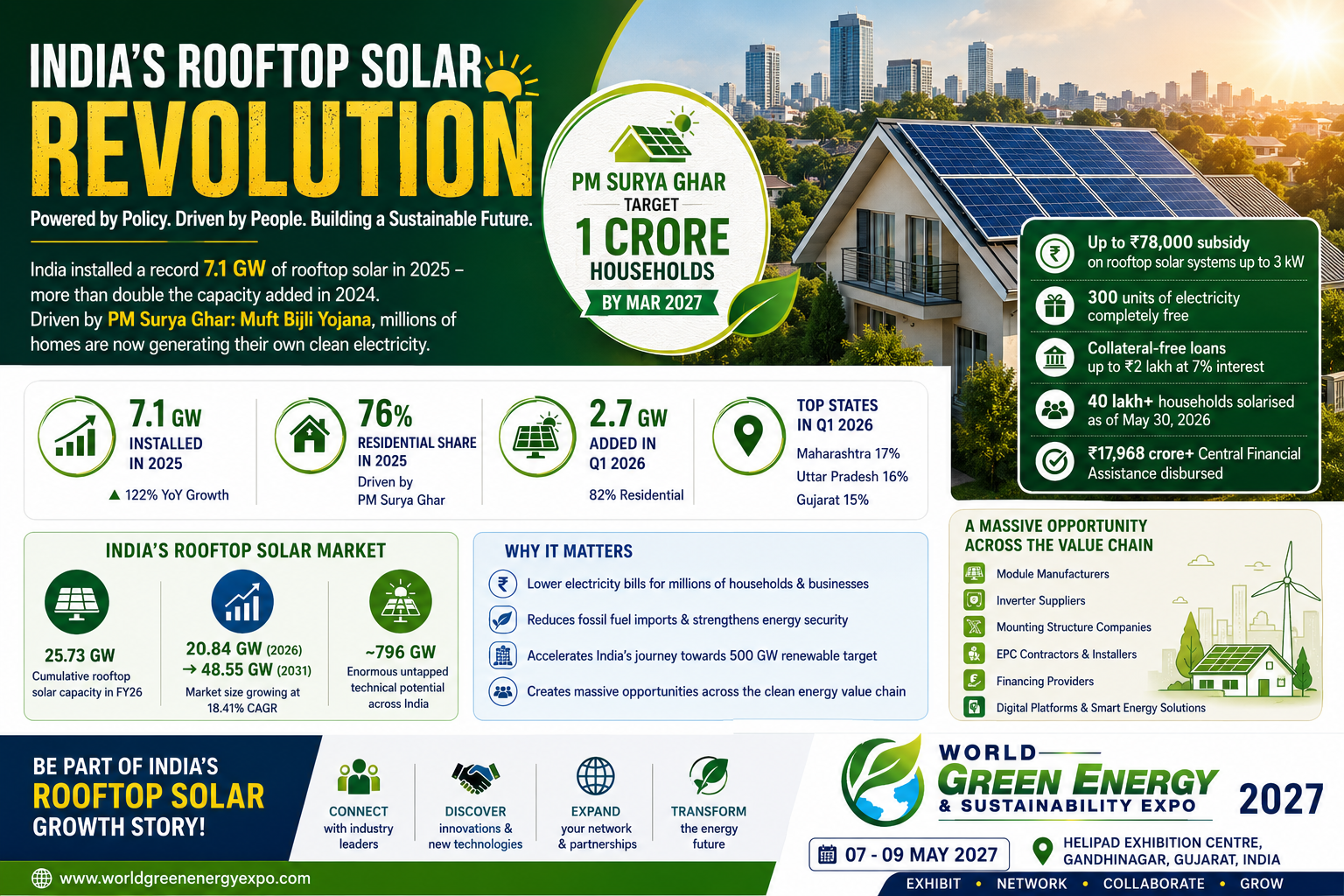

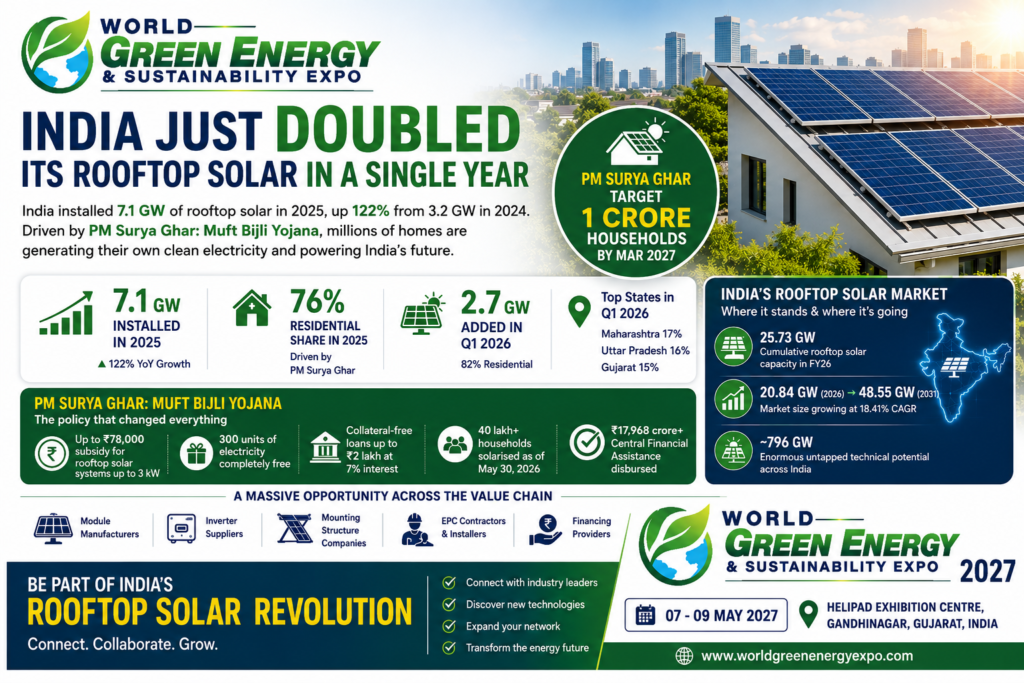

There are moments in any industry’s history when the numbers stop looking like gradual progress and start looking like a structural shift. India’s rooftop solar sector had that moment in 2025. India installed 7.1 GW of rooftop solar capacity in 2025, up 122% from 3.2 GW in 2024, according to Mercom India Research’s Q4 and Annual 2025 India Rooftop Solar Market Report. The residential sector accounted for nearly 76% of capacity additions, largely supported by the PM Surya Ghar: Muft Bijli Yojana program.

India added more rooftop solar in 2025 than it had in the previous three years combined. It did not inch forward – it doubled. And the program driving that growth, PM Surya Ghar, is still accelerating. Rooftop solar reached an all-time high of 7.1 GW in 2025, more than doubling year over year, driven largely by the PM Surya Ghar program, which accounted for a majority of installations. Strong residential adoption, streamlined subsidy disbursals, and digital approvals accelerated deployment across states.

India installed 2.7 GW of rooftop solar in Q1 2026 alone, with residential accounting for 82% of additions driven primarily by PM Surya Ghar. Maharashtra, Uttar Pradesh, and Gujarat accounted for 17%, 16%, and 15% of Q1 2026 installations respectively. What these numbers describe is not a subsidy program running its course and fading. They describe a market that has crossed a psychological and economic threshold – one where millions of Indian homeowners have decided that generating their own electricity is a sensible, affordable, and increasingly obvious financial decision.

For rooftop solar installers, module manufacturers, inverter suppliers, mounting structure companies, financing providers, and EPC contractors, this is the largest single residential energy market opportunity in Asia right now.

India’s Rooftop Solar Market Size – Where It Stands and Where It Is Going

India’s cumulative rooftop solar installations reached 20.8 GW at the end of December 2025. To understand what that number represents, consider that India’s total rooftop solar capacity was under 10 GW as recently as early 2024. The market has effectively doubled in under two years.

India’s cumulative rooftop solar capacity crossing 25.73 GW in FY26 is not merely an energy milestone – it is a structural market signal. Millions of households and enterprises have made a direct investment in their own electricity production, effectively becoming prosumers. This shift reduces forex outflow on fossil fuel imports, insulates consumers from DISCOM tariff volatility, and anchors India’s 500 GW renewable target in local, distributed infrastructure.

The forward-looking numbers are even more striking. India’s rooftop solar market size in 2026 is estimated at 20.84 GW, growing to 48.55 GW by 2031 at an 18.41% CAGR over 2026 to 2031. India’s rooftop solar potential – what could technically be installed across available roof and terrace space – dwarfs current deployment by an extraordinary margin. India has an immense, largely untapped technical potential of nearly 796 GW, with the government focusing on enabling easier financing and faster net-metering approvals to unlock this market. With 25 GW installed against 796 GW of technical potential, the Indian rooftop solar market has barely scratched the surface of what is physically possible.

The on-grid segment dominates the India rooftop solar market, holding approximately 80% market share in 2024, driven by the government’s Grid Connected Solar Rooftop Scheme and various supportive policies aimed at achieving 40,000 MW from grid-connected rooftop solar projects. On the commercial side, the India solar rooftop market generated revenue of USD 2.52 billion in 2025 and is projected to reach USD 4.27 billion by 2034. On-grid holds the largest revenue share at 90% in 2025, driven by widespread net metering adoption.

PM Surya Ghar Muft Bijli Yojana – The Policy That Changed Everything

No discussion of India’s rooftop solar market in 2027 is complete without a thorough understanding of PM Surya Ghar. This single policy intervention has restructured the residential solar market more fundamentally than anything that came before it.

With a financial outlay of INR 75,021 crore (USD 8.53 billion), the scheme targets 30 GW of residential rooftop solar capacity and coverage of 10 million households by FY2027. In just over a year since its launch, the country added 4.9 GW under PM Surya Ghar, accounting for nearly 45% of India’s total residential rooftop capacity, reaching 1.6 million households as of July 2025. Additionally, nearly 5.8 million applications had been filed under the scheme, showing that interest in rooftop solar was no longer confined to early adopters.

By early 2026, the momentum had only accelerated further. As of May 30, 2026, Union Minister Pralhad Joshi confirmed the scheme has solarised 40 lakh households, with cumulative Central Financial Assistance disbursed crossing INR 17,968 crore. The scheme’s genius lies in its simplicity and its financial directness. Under this scheme, those who install solar panels on their rooftop get 300 units of electricity completely free. The government also provides a subsidy of up to INR 78,000, which has made it much cheaper to install solar panels. The scheme aims to connect 1 crore households in the country with solar energy, with the target to be completed by March 2027. The scheme is the world’s largest domestic rooftop solar initiative with a total budget of INR 75,021 crore.

The financial model backing the scheme addresses the most fundamental barrier to residential solar adoption in India – upfront cost. The PM Surya Ghar program’s digital integration with the JanSamarth loan platform and continued improvements to the official portal enabled streamlined applications, faster approvals, and efficient subsidy disbursement. Public sector banks had approved more than 579,000 loans by September 2025.

PM Surya Ghar Subsidy Structure – The Complete 2027 Guide

Understanding the subsidy structure is essential for every solar installer, EPC contractor, and module supplier operating in the Indian residential market.

The central government subsidy under PM Surya Ghar is structured in clear slabs. For a 2-kW system, the central subsidy is INR 30,000 per kW – so INR 60,000 total. For a system between 2 kW and 3 kW, the additional kW attracts INR 18,000, bringing the total to INR 78,000 for a 3-kW system – the maximum under the central government scheme. The subsidy is paid directly to the consumer’s bank account through Direct Benefit Transfer – not to the installer – a deliberate design choice that eliminates middleman overcharging and builds consumer confidence in the program.

Combined with state-level top-up subsidies, a 3-kW system could see total subsidies exceed INR 1,00,000 in certain states. In Gujarat, the combined central and state subsidy can exceed INR 1 lakh for eligible residential installations.

For EPC companies, the subsidy disbursement request is processed by the national portal typically within 30 days of a valid commissioning certificate. The total end-to-end timeline from customer registration to subsidy receipt is typically 45 to 90 days, with most variation coming from DISCOM inspection scheduling, net metering installation timelines, and document completeness. Urban DISCOMs in states like Gujarat, Maharashtra, and Rajasthan tend toward the shorter end of this range.

The scheme also provides collateral-free financing. Easy loans of up to INR 2 lakh at 7% interest are available for systems up to 3 kW through public sector banks, with the SBI Surya Shakti Loan offering 10-year tenure. This combination of direct subsidy and collateral-free financing has brought rooftop solar within financial reach of a segment of India’s population that was previously entirely outside the market.

Industrial and commercial solar – separate but equally powerful incentives

PM Surya Ghar subsidies are exclusively for residential consumers. Industrial, commercial, and institutional consumers cannot claim this subsidy. However, industrial solar projects benefit from accelerated depreciation of 40% in year one, which provides tax savings of INR 25 to 30 per INR 100 invested – often more valuable than the residential subsidy on a per-kW basis. For a INR 4 crore solar project with 25% corporate tax rate, this means INR 40 lakh in tax savings in year one alone, with total tax benefit over the depreciation period exceeding INR 90 lakh, effectively reducing project cost by 23 to 25%.

State-by-State – Where India’s Rooftop Solar Market Is Winning

India’s rooftop solar story is not uniform across its states. Understanding the state-level landscape is critical for any company planning market entry or expansion. Rooftop solar capacity additions in 2025 were led by Maharashtra at 16%, Gujarat at nearly 16%, and Uttar Pradesh at 15%.

Gujarat – India’s Undisputed Rooftop Solar Capital

Under PM Surya Ghar, Gujarat leads all states with the highest installed residential rooftop solar capacity of 1,491 MW, followed by Maharashtra, Uttar Pradesh, Kerala, and Rajasthan. These five states together account for approximately 77.2% of total installed capacity under the scheme. Gujarat leads all states as of December 2025, with over 5.15 lakh rooftop solar systems installed and 7.41 lakh households benefited.

Gujarat’s dominance is not accidental. The state combines the most aggressive state-level solar subsidy stack in India with a progressive DISCOM structure and deep public familiarity with solar energy built over a decade of state-level promotion. Gujarat leads with its Surya Urja Rooftop Yojana, which provides an additional INR 40,000 subsidy for residential consumers on top of the central assistance. Gujarat is India’s number one state in solar adoption with over 11 lakh installations. PGVCL also covers net metering costs for consumers.

Combined, Gujarat homeowners can access total subsidies exceeding INR 1 lakh on a 3-kW system – the most generous, combined package of any Indian state – making solar genuinely affordable for virtually any homeowner with a grid connection and a suitable rooftop.

Maharashtra

Maharashtra recorded 3.92 lakh systems installed under PM Surya Ghar as of December 2025, ranking second nationally. Maharashtra launched the SMART Solar Scheme, offering an additional 40% subsidy for low-consumption homes under 100 units per month, BPL, and SC-ST households. MSEDCL group net metering allows housing societies to share solar generation across multiple flats from a single installation. Rural households with 1 to 3 kW systems also receive INR 6,000 per kW additional subsidy. Maharashtra’s group net metering innovation is particularly significant – it unlocks the enormous apartment housing society market that individual net metering rules could not serve.

Uttar Pradesh

Uttar Pradesh recorded 3.26 lakh installations under PM Surya Ghar as of December 2025, ranking third nationally. Uttar Pradesh offers an additional INR 15,000 additional incentive for SC-ST households on top of the central subsidy, administered through UPNEDA. India’s most populous state represents an enormous untapped market – with 230 million people and rapidly rising electricity consumption, UP’s addressable rooftop solar market is extraordinary in scale.

Rajasthan

Rajasthan offers INR 8,000 per kW additional state subsidy along with an expedited 15-day approval process. The state follows the Rajasthan Solar Energy Policy and allows net metering up to 1 MW. Rajasthan’s combination of high solar irradiance, progressive net metering policy, and fast approval process makes it one of the most commercially attractive states for rooftop solar EPC companies.

Kerala

Kerala recorded 1.77 lakh installations under PM Surya Ghar as of December 2025, ranking fourth nationally. KSEB provides a free technical site inspection and an additional INR 5,000 subsidy for women-owned homes. Kerala offers its own separate solar subsidy schemes that are time-bound and based on availability. Kerala’s high electricity tariffs and strong consumer awareness make economics exceptionally compelling for residential solar buyers.

Tamil Nadu

Tamil Nadu’s TANGEDCO reduces the net meter installation fee to zero for solar systems below 5 kW. While Tamil Nadu does not stack a separate state subsidy as of 2026, TEDA coordinates fast approvals and the state has a well-developed solar installation ecosystem. Tamil Nadu has the highest installed rooftop solar capacity in India when including both pre-scheme installations and PM Surya Ghar additions – a reflection of a market that developed strong commercial and industrial rooftop solar penetration before the residential program launched.

Who Is Driving Growth – The Segment-by-Segment Picture

The residential sector accounted for nearly 76% of rooftop capacity additions in 2025, largely supported by PM Surya Ghar. Industrial, commercial, and government segments contributed 18%, 5%, and 1% respectively. Installations under the capital expenditure model represented 85% of the year’s total, while operational expenditure or RESCO installations made up 15%. The residential segment’s dominance represents a structural reversal from how this market looked just three years ago. Residential installations, which made up only a third of rooftop solar three years ago, now account for 75% of the market. This trend is expected to continue until the PM Surya Ghar target is reached.

The commercial and industrial segment, though currently smaller as a proportion, carries very strong fundamentals of its own. The demand from commercial and industrial entities remains consistent as electricity cost savings through rooftop solar is time-tested. Industrial tariffs of INR 10 to 13 per kWh in states like Maharashtra make solar savings enormous for industrial consumers. For EPC contractors and system integrators, the C&I segment offers larger average project sizes, more predictable procurement processes, and less dependence on subsidy timelines.

The RESCO or opex model – where consumers pay for solar power rather than owning the system – is also growing as an alternative to the capex model, particularly for commercial and industrial buyers who prefer an operating expense rather than capital investment structure. Models such as loans, leasing arrangements, and power purchase agreements are improving affordability and enabling wider participation among households and small enterprises. This trend gained momentum in 2025 when Tata Power Renewable Energy introduced EMI-based rooftop solar solutions in Bhubaneswar under its Ghar Ghar Solar campaign, supported by central and Odisha state subsidies.

The ALMM and DCR Challenge – What Every Company Must Understand

The regulatory landscape for rooftop solar in India changed in a fundamental and commercially significant way in 2026, and any company operating or planning to enter this market must understand the implications. From June 1, 2026, the ALMM List II requirement – mandating that solar cells used in modules supplied for government-supported projects must be from ALMM-listed domestic manufacturers – came into force. This sits alongside the existing Domestic Content Requirement for PM Surya Ghar subsidy eligibility.

The domestic content requirement policy aims to boost local manufacturing, but domestic cell capacity of 25 GW lags far behind the 100-plus GW module capacity. DCR-compliant modules cost INR 23 to 26 per watt, nearly double non-DCR imports, prompting many consumers to forgo subsidies for cheaper and faster installations. ALMM List II enforcement and rising DCR module prices could lead to higher system costs. Sustaining growth will depend on maintaining cost competitiveness and ensuring smooth execution as compliance requirements increase.

For module manufacturers, this creates a powerful incentive to expand domestic cell manufacturing capacity as rapidly as possible – since ALMM-listed modules command a significant price premium in the subsidized residential market. For EPC contractors, this means a thorough understanding of ALMM compliance is no longer optional – it is a basic commercial requirement for any company bidding on PM Surya Ghar projects.

ALMM listing and DCR compliance – both are mandatory for subsidy eligibility. Monocrystalline PERC panels are recommended for 2026 due to higher efficiency at 22-plus percent and superior performance in lower light. Bifacial Mono PERC panels offer enhanced generation by using both sides. Capacity of 550W to 590W modules is the current standard, reducing the total number of panels needed compared to older 400W modules.

The Companies Leading India’s Rooftop Solar Market

India’s rooftop solar supply chain spans module manufacturers, inverter suppliers, system integrators, installation companies, and financing platforms – each playing a distinct and essential role.

On the module supply side, ALMM-listed manufacturers including Waaree Energies, Adani Solar, Tata Power Solar, Vikram Solar, and Goldi Solar dominate residential procurement. Vikram Solar’s ALMM-listed modules have earned Kiwa PVEL Top Performer recognition for seven consecutive years. In April 2026, the company crossed 10 GW in cumulative global solar module deployments, having doubled its installation base from 5 GW to 10 GW in just two years – equivalent to over 25 million solar modules powering more than 5 million Indian homes.

On the rooftop installation and EPC side, the major companies operating in the India rooftop solar market include Tata Power Solar Systems, Amplus Solar Power, CleanMax Enviro Energy Solutions, Orb Energy, and Sunsource Energy. Tata Power Solar has built the largest residential rooftop installation track record in India – over 1.5 GW of cumulative rooftop installations — through its Ghar Ghar Solar campaign and extensive national installer network.

SolarSquare has emerged as one of the most aggressive residential solar installation brands. In 2025, SolarSquare launched its nationwide Apna Desh, Apni Bijli campaign aligned with PM Surya Ghar and Atmanirbhar Bharat, reporting support for over 30,000 families across more than 20 cities through residential rooftop installations. Amplus Solar, CleanMax, and Sunsource Energy dominate the commercial and industrial open-access rooftop segment, delivering multi-megawatt installations for factories, warehouses, data centres, and commercial campuses across India.

On the financing side, by leveraging Redington’s distribution network and enabling access to subsidies of up to INR 78,000 under PM Surya Ghar, various initiatives are accelerating market penetration and household adoption. The JanSamarth portal integration with PM Surya Ghar has made collateral-free solar loans from over 15 public sector banks accessible through the same digital journey as the subsidy application.

The Real Challenges and Where the Market Gaps Are

A credible assessment of India’s rooftop solar market cannot ignore the genuine implementation challenges that slow down what would otherwise be an even faster expansion.

Just 22.7% of applications have translated into completed installations, reflecting bottlenecks in financing, vendor capacity, and approvals. With 5.8 million applications filed and only 1.3 million systems installed as of mid-2025, there is an enormous pipeline of intent that has not yet converted into physical panels on rooftops. This conversion gap is, frankly, one of the most significant business opportunities in the entire Indian solar market – for companies that can streamline installation, simplify financing, and improve the consumer journey from application to commissioning.

Portal and DISCOM coordination remains uneven across states. Frequent errors on the National Portal for Rooftop Solar and weak complaint tracking delay subsidies and strain trust. Vendor concentration in a few states causes delivery delays elsewhere. Inconsistent installation quality persists despite MNRE’s certification drive.

Net metering policy inconsistency is another friction point. While net metering is mandated nationally under the Electricity Rights of Consumers Rules 2020, implementation varies considerably across DISCOMs. Some states process net meter applications in days; others take months. This inconsistency directly affects the financial return calculation that homeowners use to decide whether to install solar – and a slow net metering process can kill a sale even when every other factor is favorable.

Scaling rooftop solar beyond 25 GW will depend on the alignment of regulatory frameworks, financing ecosystems, and distributed energy infrastructure at scale. Over the next five years, progress will hinge on institutional catch-up, with DISCOMs, state agencies, banks, and the installer ecosystem scaling in step with the political ambition already embedded in the grid transition. For companies with solutions in digital consumer onboarding, DISCOM integration software, quality assurance and monitoring systems, and distributed workforce management, these friction points are not just operational challenges – they are addressable market opportunities worth hundreds of crores annually.

The Business Opportunity – What This Market Means Segment by Segment

The rooftop solar revolution creates distinct and sizeable business opportunities across multiple value chain segments simultaneously.

For module manufacturers

Rooftop solar tenders totaling 3.8 GW were issued in 2025, a 32% rise from the previous year. Each gigawatt of residential rooftop installation requires approximately 1.8 to 2 million individual solar modules. At current run rates, India’s residential rooftop market alone is consuming upward of 12 to 14 million modules annually – and growing.

For inverter manufacturers

Every rooftop solar system requires at least one inverter. The shift toward hybrid inverters – which combine solar generation, grid connection, and battery storage management in a single unit – is accelerating as homeowners seek backup power alongside savings. Battery-solar hybrid and IoT-based rooftop management innovations will add significant momentum to inverter demand and average selling prices over the coming years.

For mounting structure companies

The residential rooftop market requires lightweight, corrosion-resistant, easy-to-install mounting systems suited to a wide variety of Indian roof types – RCC flat roofs, corrugated metal sheets, clay tiles, and concrete slabs. Companies with modular, installer-friendly mounting systems that reduce installation time have a direct competitive advantage in a market where installation labor cost and timeline are key purchasing criteria.

For EPC contractors and solar installers

Based on current daily installation rates trending toward 100,000 meters per day, India will install approximately 30 to 36 crore additional smart meters between 2026 and 2030. The parallel rooftop solar installation pipeline – millions of residential systems, thousands of commercial rooftop projects, and hundreds of industrial installations – requires a national network of trained, quality-certified solar EPC contractors that is still well short of what the market needs. Companies that invest in installer training, quality certification, and DISCOM relationship management are capturing a structurally undersupplied segment of this market.

For financing companies and fintech platforms

The expansion of innovative financing options that reduce upfront investment barriers for individuals is a crucial factor bolstering market growth. EMI-based solar financing, solar loans integrated with subsidy disbursement, and RESCO structures for commercial buyers are all growing rapidly. The intersection of financial product design and solar market penetration is one of the most commercially fertile areas in the entire Indian clean energy ecosystem right now.

Why World Green Energy & Sustainability (WGES) Expo 2027 Is the Right Platform for India’s Rooftop Solar Industry

Every segment of the rooftop solar value chain profiled above – module manufacturers, inverter suppliers, mounting structure companies, EPC contractors, financing providers, and digital platform developers – is either already exhibiting at World Green Energy & Sustainability (WGES) Expo 2027 or evaluating whether to.

Gujarat, the host state of World Green Energy & Sustainability (WGES) Expo 2027, is India’s undisputed rooftop solar capital. Gujarat leads with over 11 lakh solar installations nationally, benefits from the most generous, combined subsidy package of any Indian state and has PGVCL covering net metering costs for consumers. The state’s combination of policy generosity, installation scale, and manufacturing concentration – Waaree, Goldi Solar, and Adani Solar all have major manufacturing facilities in Gujarat – means the entire rooftop solar supply chain ecosystem sits within a few hours of the World Green Energy & Sustainability (WGES) exhibition venue.

For international module manufacturers targeting India’s DCR and ALMM-compliant market through local manufacturing partnerships, World Green Energy & Sustainability (WGES) Expo 2027 is where Indian manufacturing partners are found. For rooftop EPC companies seeking module and inverter supply agreements for their growing residential pipelines, World Green Energy & Sustainability (WGES) Expo 2027 is where supplier conversations happen face to face. For inverter and mounting structure companies seeking empaneled vendor relationships with India’s growing network of MNRE-certified installers, World Green Energy & Sustainability (WGES) Expo 2027 is the most direct route.

And for any company that has been watching India’s rooftop solar numbers from the outside and wondering when to enter – the answer that the 2025 data suggests is: the market is already large, it is still accelerating, and the companies establishing supply chain, distribution, and installation network relationships in 2027 will be the ones with structural advantages when the market crosses 40 GW and 50 GW in the years that follow.

Register as an exhibitor at the World Green Energy & Sustainability (WGES) Expo 2027 today. Secure your position in front of India’s most active solar buyers, developers, investors, and policymakers – all in one place, at the moment the market is moving fastest.

For more details: contact us at info@adexexhibitions.com | +91 81770 53335 | +91 91528 96078

For Exhibitor Registration: If you have not registered, you may also fill out this Exhibitor Registration Form.