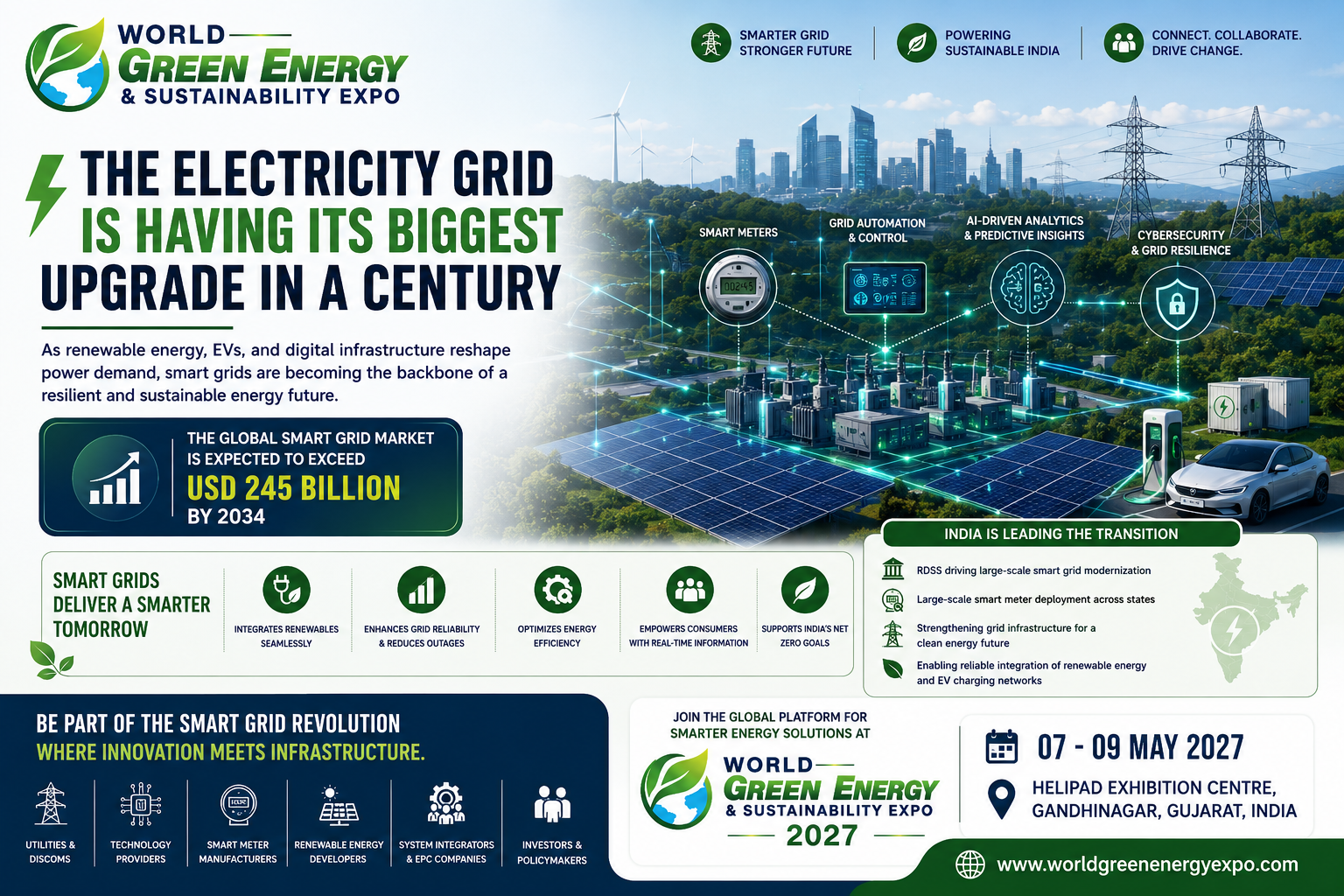

The Electricity Grid Is Having Its Biggest Upgrade in a Century

The electricity grid most countries run on today was designed for a world that no longer exists.

It was built to move power in one direction – from large coal or gas power plants down through transmission lines to homes and factories. It was designed when electricity demand was predictable, when there were no solar panels on rooftops sending power back up the line, when nobody expected the grid to charge millions of electric vehicles overnight, and when cybersecurity was not a consideration because the grid had no digital components worth attacking.

That world ended somewhere around 2015. The grid it left behind is now visibly struggling to keep up. The global surge in energy demand, driven by urban expansion, industrial growth, and increased electrification of transportation, places immense pressure on existing power grids – many of which were built decades ago and are ill-equipped to manage modern energy loads, resulting in frequent outages, voltage fluctuations, and transmission inefficiencies.

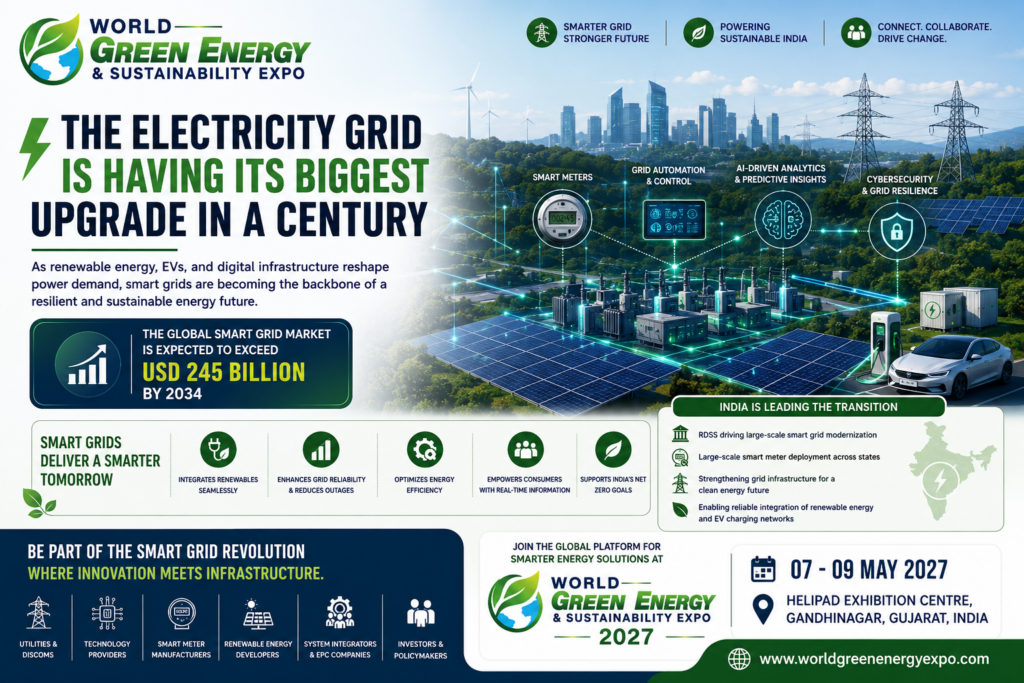

The answer to this problem is what the industry calls a smart grid – an electricity network rebuilt around digital communication, real-time data, and two-way energy flow. And the scale of global investment now flowing into this technology transformation is genuinely staggering. The smart grid technology market grew from USD 63.67 billion in 2025 to USD 75.99 billion in 2026 at a CAGR of 19.3% and is projected to reach USD 154.37 billion by 2030 at a continued CAGR of 19.4%.

For smart meter manufacturers, grid automation companies, distribution management system providers, IoT energy platform developers, cybersecurity specialists, and communication technology firms, smart grid modernization is not a future market. It is the largest single infrastructure spending category in the global energy sector right now – and it is accelerating, not plateauing.

How Big Is the Smart Grid Market in 2027 – And How Fast Is It Growing?

Market sizing for smart grids varies across research houses depending on which components they include, but every credible forecast agrees on two things: the market is already enormous, and it is growing at a pace that puts almost every other infrastructure category in the shade. The global smart grid market size was USD 61.05 billion in 2025 and is projected to grow from USD 74.72 billion in 2026 to USD 245.60 billion by 2034 at a CAGR of 16.04%.

Other research houses arrive at slightly higher absolute figures depending on methodology. The global smart grid market was valued at USD 66.3 billion in 2024 and is projected to grow from USD 77.97 billion in 2025 to USD 285.22 billion by 2033, growing at a CAGR of 17.6% from 2026 to 2033. Global smart grid market size is valued at USD 86.4 billion in 2025 and is projected to grow at a CAGR of 16.9% during the forecast period, reaching USD 301.0 billion by 2033.

What is consistent across every source is the direction and the pace. A market that was roughly USD 60 to 80 billion in 2025 is headed toward USD 245 to 300 billion within a decade – a tripling in less than ten years. This is what a genuinely structural infrastructure upgrade cycle looks like when it kicks into full gear simultaneously across the world’s largest economies.

Smart grid spending is shifting from pilots to programs as utilities chase resilience, faster interconnection, and controllable capacity. Global electricity demand is expected to grow by an average of 3.4% annually through 2026, and this demand acceleration strengthens the business case for smart grid rollouts because the system needs more flexible distribution operations, tighter congestion management, and faster interconnection. McKinsey’s analysis of the data centre buildout projects global data-centre power demand reaching 1,400 TWh by 2030, or roughly 4% of total global electricity demand – adding an entirely new category of premium power reliability demand that conventional grids simply cannot serve without digital intelligence.

North America dominated the smart grid market with a market share of 30.91% in 2025, standing at USD 18.87 billion and is projected to grow to USD 22.8 billion in 2026. Asia-Pacific is expected to expand at the fastest CAGR during the forecast period, with nations like China, Thailand, and India providing lucrative growth opportunities owing to increasing government initiatives and investments.

What a Smart Grid Actually Does – And Why It Matters for Renewable Energy

Understanding why this market is growing so fast requires understanding what a smart grid actually changes, not just in engineering terms but in economic terms.

A smart grid is an advanced electricity supply network that utilizes digital communications technology to identify the demand of electricity in real-time, react to local changes in usage, and enable the network to self-heal automatically in case of a power disturbance. It is an intelligent overlay to the existing electrical grid network with advanced feedback alternatives such as active network management systems and demand response management systems. The highly interconnected network uses meters, sensors, digital controls, and analytic tools to monitor, automate, and control energy flow.

For renewable energy specifically, the smart grid is not a nice-to-have enhancement. It is a technical prerequisite for operating a grid with high proportions of solar and wind generation. Growth in the smart grid technology market is attributed to the expansion of AI-driven grid analytics, growth of renewable energy integration, deployment of advanced demand response systems, modernization of aging grid infrastructure, and adoption of wireless communication technologies for grid monitoring.

Every time a solar panel generates surplus power on a sunny afternoon, a smart grid can redirect that surplus to where it is needed, store it in a battery system, or signal demand-response systems to increase consumption in factories and commercial buildings at that precise moment. Without that intelligence, surplus solar generation either goes to waste or destabilizes grid frequency. With it, renewable generation becomes a managed, dispatchable resource rather than an unpredictable variable.

The technology components making this possible span a wide range. The advanced metering infrastructure segment dominated the global smart grid market in 2025 in terms of revenue, attributed to the increasing adoption of smart meters across the globe. The distribution segment is estimated to be the most opportunistic segment during the forecast period, driven by the rising adoption of cloud computing and improvements in distribution management systems.

The smart grid sector from distribution and network automation technologies is anticipated to reach more than USD 50 billion by 2034, while the support and maintenance services segment was valued at over USD 19 billion in 2024, driven by the rising focus on predictive maintenance and monitoring to improve grid reliability.

Global Investment – The Countries Writing the Biggest Cheques

The scale of national government investment in smart grid infrastructure is unlike almost any previous energy infrastructure program, because it is happening simultaneously across every major economy rather than sequentially.

According to IEA data, the European Union plans to invest USD 1.2 billion in its electricity grid by 2030, with USD 3.6 billion earmarked specifically for digitalization of power grids. China is aiming to invest USD 50 billion from 2021 to 2025 to modernize its grids. Japan has announced a USD 20 billion funding program, while India has launched a USD 38 billion scheme to enhance power distribution. The Grid Resilience Innovative Partnership program, with USD 10.5 billion in funding, has been introduced in the United States, while Canada is supporting smart grid deployment with USD 100 million through its Smart Grid Program.

Investment in electricity grids increased by 8% in 2022, with major economies making significant commitments. The EU plans to invest USD 633 billion by 2030, China plans to invest USD 442 billion by 2025, Japan plans to invest USD 155 billion, India plans to invest USD 36.8 billion, and the US plans to invest USD 10.5 billion.

China’s state grid owner has targeted over CNY 4 trillion, approximately USD 574 billion, of investment over 2026 to 2030, averaging roughly CNY 800 billion per year. This frames China as a sustained demand centre for grid equipment, digital substations, dispatch modernization, and long-distance transmission integration.

Europe’s distribution grid investment averaged approximately EUR 33 billion per year between 2019 and 2024 and is estimated to need to rise to approximately EUR 67 billion per year between 2025 and 2050 to deliver electrification and integration goals. That doubling of annual investment is not aspirational – it is what Europe’s own grid operators have identified as the minimum needed to connect offshore wind, accommodate electric vehicle charging, and integrate distributed rooftop solar without destabilizing national grids.

The smart grid ecosystem shows a mature and well-capitalized investment landscape, with an average investment value of USD 51.8 million per funding round, and more than 2,600 investors actively participating in the ecosystem, which shows broad institutional and strategic interest in grid modernization and digital infrastructure.

India’s Smart Grid Revolution – The World’s Most Ambitious Metering Program

India’s approach to smart grid modernization is unlike any other country’s – in both its ambition and its complexity. The centre piece of India’s grid modernization effort is the Revamped Distribution Sector Scheme, universally known as RDSS. Launched in July 2021, the RDSS has earmarked INR 97,631 crore for prepaid smart meters and another INR 1.8 lakh crore for strengthening distribution infrastructure. Its headline goals are clear: reduce nationwide AT&C losses to 12 to 15 percent, eliminate the ACS-ARR gap, and install 250 million smart meters by financial year 2027 to 2028 after a two-year extension of the original deadline.

RDSS has seen approvals for projects worth INR 2.83 lakh crore. Of this, INR 1.53 lakh crore has been allocated for loss reduction infrastructure while INR 1.31 lakh crore is dedicated to smart metering initiatives. Projects covering 20.33 crore smart meters have been sanctioned, including meters for 19.79 crore consumers, 2.11 lakh feeders, and 52.53 lakh distribution transformers.

The deployment progress has been genuinely rapid once implementation challenges were addressed. India has crossed a significant milestone with 3.46 crore smart electricity meters installed across the country as of June 30, 2025. Out of the total installed meters, 2.27 crore were deployed under RDSS.

The speed of installation is accelerating sharply. At present, around 80,000 smart meters are being installed per day in India. In the coming period, this is expected to reach 100,000 per day. Based on current daily installation rates of approximately 80,000 per day in late 2025, trending toward 100,000 per day, India will install approximately 30 to 36 crore additional meters between 2026 and 2030. Combined with existing installations, total smart meter penetration could reach 35 to 40 crore by 2030 – approximately 90 to 100 percent of the RDSS target.

The financial results of this modernization are already measurable and significant. AT&C losses, which reflect the gap between electricity supplied and revenue realized, have dropped from 21.91 percent in FY21 to 16.12 percent in FY24, a decline credited to reforms under RDSS and other policy initiatives. Billing efficiency rose from 84.08% in FY21 to 87.59% in FY25, and collection efficiency increased from 92.9% to 97% during the same period.

The scale of what remains to be installed is, if anything, the more commercially significant number for any company considering the Indian market. Smart metering is not optional in India’s energy vision – it is the foundational data layer without which none of the grid intelligence, demand flexibility, EV management, and distributed energy integration goals are achievable. The RDSS, in this context, is not just a loss reduction scheme – it is India’s investment in the digital nervous system of its future energy economy. India’s smart metering program is simultaneously the world’s most ambitious and most instructive energy infrastructure undertaking. Its ambition – 25 crore meters in five years, financed through an innovative TOTEX-AMISP model, on the back of the world’s most complex distribution system – is without global parallel.

For smart meter manufacturers, communication technology suppliers, AMI software providers, and grid analytics companies, the Indian market offers a procurement pipeline that is both enormous in scale and actively accelerating in pace.

Country-by-Country – How Major Economies Are Modernising Their Grids

United States

The US smart grid market size reached USD 12.54 billion in 2025 and is projected to be worth USD 57.32 billion by 2035, at a CAGR of 16.41%. The US Department of Energy has introduced smart grid grants providing over USD 600 million per year between 2022 and 2026. The United States plays a leading role in North America’s smart grid market through large-scale investments in grid modernization, federal funding programs, and strong policy support. Initiatives like the Grid Resilience and Innovation Partnership enhance grid reliability and renewable integration.

China

China’s state grid owner has targeted over CNY 4 trillion, approximately USD 574 billion, of investment over 2026 to 2030, averaging roughly CNY 800 billion per year, framing China as a sustained demand centre for grid equipment, digital substations, dispatch modernization, and long-distance transmission integration. China leads the world in smart meter penetration, with over 500 million smart meters already deployed across its national grid – the largest installed base of any country.

European Union

Eurelectric’s investment benchmark shows Europe’s distribution grid investment averaged approximately EUR 33 billion per year from 2019 to 2024 and must rise to approximately EUR 67 billion per year between 2025 and 2050 to deliver electrification and integration goals. This represents a strong capital expenditure gap connecting directly to smart grid themes like automation, flexibility markets, and digital grid management. Germany, France, the Netherlands, and the Nordic countries are the most advanced in smart meter deployment and distribution automation within the EU.

Japan

Japan has announced a USD 20 billion funding program for grid modernization. Japan has achieved near-universal smart meter coverage in its urban grid, with over 80 million smart meters installed across the country. Its focus has shifted from deployment to analytics – extracting the maximum economic value from the data these meters generate.

Middle East

Saudi Arabia, the UAE, and Qatar are making significant investments in smart grid infrastructure as part of their broader economic diversification away from fossil fuel dependency. The UAE’s smart grid program – targeting zero carbon in its power sector by 2050 – requires a complete overhaul of distribution infrastructure, creating major procurement opportunities for international smart grid technology companies.

Southeast Asia

Vietnam, Indonesia, Thailand, and the Philippines are all at early but rapidly accelerating stages of smart meter and grid automation deployment. The combination of rapidly growing electricity demand, significant grid losses, and government renewable energy targets makes Southeast Asia one of the most compelling emerging markets for smart grid technology companies in 2027.

The Technology Stack – What a Modern Smart Grid Is Actually Made Of

Understanding the technology components of a smart grid is essential for any company looking to position its products or services in this market.

Advanced Metering Infrastructure, or AMI, is the foundation layer. The deployment of advanced metering infrastructure and smart sensors is one of the primary drivers of smart grid market growth, enabling governments and utilities to invest heavily in digital grid technologies to enhance energy efficiency, reduce transmission losses, and improve grid resilience against outages and cyber threats. AMI is not simply a meter replacement program – it is a two-way communication network connecting every electricity endpoint to a central data management system, enabling remote reading, real-time consumption monitoring, dynamic tariffs, and automated demand response.

Distribution Management Systems, or DMS, use real-time data from sensors and meters to optimize power flow across the distribution network, automatically rerouting power around faults, balancing load across feeders, and integrating distributed energy resources like rooftop solar into the grid without destabilizing frequency or voltage.

SCADA, or Supervisory Control and Data Acquisition systems, provide real-time monitoring and control of high-voltage transmission infrastructure. Modern SCADA systems increasingly incorporate machine learning to predict equipment failures before they happen and cybersecurity layers to protect against the rapidly growing threat of grid-targeted cyberattacks.

Energy Management Systems, or EMS, operate at the building and facility level – allowing industrial plants, commercial buildings, and large campuses to manage their own energy consumption intelligently in response to grid price signals, demand response incentives, and self-generated solar or storage capacity.

IoT sensors deployed across substations, distribution transformers, and transmission towers provide the real-time condition monitoring data that turns preventive maintenance into predictive maintenance – replacing the old approach of repairing equipment after it fails with a data-driven approach of replacing components before they fail.

AI and machine learning are increasingly being integrated at every layer of this technology stack. GE Vernova in July 2025 announced the acquisition of French AI firm Alteia to enhance its GridOS Visual Intelligence platform. This integration enables AI-powered analysis of visual and operational data, improving smart grid asset monitoring, predictive maintenance, and infrastructure reliability for utility providers globally.

Communication technology underpins all of it. The development of cloud computing, IoT, and automation, as well as the growing need for digital transformation and the ability to scale enterprises will increase the need for smart grid services. The communication technologies connecting smart meters, sensors, and control systems span Power Line Communication, RF mesh, cellular 4G and 5G, fibre optic, and satellite – with different technologies suited to different network densities and geographic conditions.

The Companies Leading the Smart Grid Industry

The smart grid competitive landscape spans large industrial conglomerates with decades of power systems experience, technology companies that have entered the grid from the IT and telecommunications side, and a fast-growing tier of specialist startups addressing specific digital intelligence niches.

The global smart grid market is highly competitive, with key players like Siemens, General Electric, ABB, Schneider Electric, and Hitachi Energy leading innovation. Siemens focuses on digital grid solutions and AI integration, while GE Vernova is expanding through acquisitions like Alteia to enhance visual intelligence. Schneider Electric emphasizes smart energy management systems. These companies compete through strategic partnerships, technological advancements, and regional expansions to strengthen their global smart grid market presence.

Siemens AG

Siemens AG is one of the most comprehensive smart grid technology companies globally, offering everything from high-voltage substation automation to distribution management software, smart meter communication systems, and AI-driven grid analytics. Its partnership with multiple Indian state utilities positions it well for India’s RDSS-driven modernization.

ABB Ltd

ABB Ltd operates across the full smart grid value chain including power transformers, high-voltage direct current transmission, distribution automation, and energy management software. In January 2025, ABB and Škoda Group formed a partnership for railway electrification, with ABB supplying its Traction Battery Pro Series to power Škoda’s new fleet of battery-electric multiple units – an example of how smart grid companies are extending into adjacent electrification markets.

Schneider Electric

Schneider Electric leads the global market in energy management systems and distribution automation software. Its EcoStruxure platform – connecting smart meters, distribution automation, and building energy management into a unified data platform – is widely deployed across utilities, industrial facilities, and commercial buildings globally.

GE Vernova

GE Vernova brings decades of power generation, transmission, and grid control system experience into the smart grid market, reinforced by its 2025 acquisition of Alteia for AI-powered visual grid intelligence.

Itron

Itron is the world’s leading specialist in smart metering hardware and AMI communication systems. Its smart meters and communication networks are deployed across utilities in North America, Europe, Asia, and increasingly India as global AMI programs accelerate.

Cisco Systems

Cisco Systems brings enterprise networking and cybersecurity expertise into grid infrastructure. In February 2025, Cisco introduced a new family of Smart Switches integrating networking and security into a compact solution, powered by AMD Pensando DPUs, which simplify data centre design and enhance efficiency, addressing the growing complexity of AI workloads by enabling automated and predictive operations.

Hitachi Energy

Hitachi Energy – the combined grid technology business of Hitachi and ABB’s former power grids division – is a significant force in HVDC transmission, power quality, and grid automation across Asia, Europe, and North America.

Wipro & IBM

Wipro and IBM represent the technology services dimension of smart grid – providing the systems integration, data analytics, cloud platform, and cybersecurity services that utilities need to make their smart grid hardware investments actually deliver value through operational intelligence.

In India specifically, domestic companies including Genus Power, Secure Meters, L&T Technology Services, and Tata Consultancy Services have built significant positions in smart metering hardware, AMI communication systems, and grid management software, competing directly with international players for RDSS contracts.

The smart grid ecosystem spans approximately 700 smart grid startups within a broader ecosystem of 5,000 total companies. Activity concentrates across leading country hubs including the US, India, the UK, Germany, and the Netherlands. Major city hubs such as London, Bangalore, New York City, Berlin, and Dubai anchor deployment, innovation, and investment across global smart grid markets. Bangalore’s position in this list is notable – India’s technology capital is increasingly a global hub for smart grid software development and systems integration, attracting both domestic and international talent into the sector.

The Real Challenges Facing Smart Grid Deployment

An honest assessment of this market cannot ignore the genuine challenges that slow down deployment even when policy intent and investment commitment are strong.

Cybersecurity risk is the most serious structural concern. A smart grid that connects millions of meters, sensors, and control systems through digital networks is also a smart grid that presents an enormous attack surface for adversaries seeking to disrupt electricity supply. High-profile grid cyberattacks in Ukraine, the United States, and India have demonstrated that this is not a theoretical risk. Governments and utilities are investing heavily in digital grid technologies to improve grid resilience against outages and cyber threats – but the investment in grid cybersecurity is still widely regarded as insufficient relative to the expanding digital attack surface.

Interoperability and standards fragmentation remain a persistent headache. Smart grid systems from different vendors – meters, communication networks, distribution management software, energy management systems – must exchange data seamlessly to deliver their full value. In practice, proprietary standards and incompatible communication protocols continue to create integration costs and delays that eat into the economic case for individual technology investments.

The analytics gap in India deserves specific mention. International experience shows analytics must be planned before meter installation. Successful global AMI deployments in the Netherlands, Finland, and the US started analytics 18 to 24 months prior to meter rollout. India’s RDSS installed meters first and is building analytics later – costing years of learning and loss reduction. The current less than 2% prepaid activation rate is the most important gap between installation and impact. For grid analytics software companies, this gap is simultaneously a challenge and a significant commercial opening – the demand for analytics capability to make India’s installed meter base fully productive is substantial and growing.

Consumer engagement is an underappreciated challenge. Smart meters and demand response systems only deliver their full economic value when consumers actively engage with the price signals and usage data they provide. Designing the consumer interface, rate structures, and communication strategies that actually change energy behavior – rather than simply installing meters that are technically capable of enabling behavior change – is where many smart grid programs have struggled.

Why World Green Energy & Sustainability (WGES) Expo 2027 Is Where the Smart Grid Industry Meets India’s Biggest Buyers

Smart grid technology, in its full scope, touches almost every exhibitor category at World Green Energy & Sustainability (WGES) Expo 2027. Smart meters are directly relevant to every solar project that installs rooftop panels under PM Surya Ghar. Grid automation is directly relevant to every utility-scale solar and wind developer seeking grid interconnection. Energy management systems are directly relevant to every industrial company seeking to manage its energy costs under open-access renewable energy structures.

Gujarat – the host state of World Green Energy & Sustainability (WGES) Expo 2027 — is itself one of India’s most active smart grid markets. With some of the country’s most progressive DISCOM structures, a leading position in rooftop solar under PM Surya Ghar, and direct proximity to India’s largest renewable energy development corridor from Kutch to Rajasthan, Gujarat’s grid modernization investment is among the highest of any Indian state.

For smart meter manufacturers targeting India’s 20.33 crore sanctioned but still-to-be-installed meters, for AMI communication technology companies competing for RDSS contracts, for distribution management software providers seeking DISCOM partnerships, for grid cybersecurity companies entering the Indian utility market, and for IoT sensor and edge computing companies targeting India’s substation modernization program – World Green Energy & Sustainability (WGES) Expo 2027 is where the procurement decision-makers, state DISCOM representatives, MNRE officials, and renewable energy developers who are reshaping India’s grid are all present at the same time.

This is the platform where smart grid conversations meet solar deployment reality, and where international grid technology companies meet the Indian distribution utilities and energy companies who are spending INR 2.83 lakh crore on exactly the technology they offer.

Register as an exhibitor at the World Green Energy & Sustainability (WGES) Expo 2027 today. Secure your position in front of India’s most active solar buyers, developers, investors, and policymakers – all in one place, at the moment the market is moving fastest.

For more details: contact us at info@adexexhibitions.com | +91 81770 53335 | +91 91528 96078

For Exhibitor Registration: If you have not registered, you may also fill out this Exhibitor Registration Form.